Macroeconomic Goal: Economic

Growth

Introduction

Review: What do we already know about Economic Growth?

Economic Growth from the 5Es lesson:

Economic Growth is one of the "5 Es" of economics or one of the

five ways for a society to reduce scarcity.

We defined Economic Growth as an increase in the ABILITY to

produce goods and services and we noted that this not the way the

term is normally defined.

This type of Economic Growth is caused by:

a) more resources

b) better resources

c) better technology

If we only had more resources we could produce more goods and

services and satisfy more of our wants. This will reduce scarcity

and give us more satisfaction (more good and services). All

societies therefore try to achieve economic growth.

In the AS-AD chapter we redefined this type of growth as

"increasing the potential" level of output.

Economic Growth from Production Possibilities lesson

We used the production possibilities model to demonstrate

how economic growth can reduce scarcity.

We can increase our ABILITY to produce goods and services (or

increase our POTENTIAL GDP) if we get:

- more resources

- better resources, and

- better technology

Since this increase maximum output that we are able to produce

it shifts the production possibilities curve outward. On the graph

below, economic growth would cause the production possibilities

curve to move from PP1 to PP2.

If we have more resources we are able to produce more

and therefore the maximum amount that can be produced (i.e. the

production possibilities curve) increases.

This doesn't necessarily mean that the economy IS producing

more, just that it CAN produce more. To achieve our new

potential levels of output we also need full employment and

productive efficiency. It could be possible to have this type

of economic growth so that we CAN produce the quantities

represented by point E, but if there is unemployment and

productive inefficiency we would be at a point beneath this new

curve (maybe point C). So we may get new resources or new

technology so we CAN produce more (point E on PP2), but if we

don't use the new resources (i.e. we have unemployment) or if

we don't use the new technology (i.e. we have productive

inefficiency) , we may remain on PP1 (point C).

Economic Growth from the AS - AD Lesson:

In the chapter on AS-AD we introduced three different

definitions of economic growth:

- INCREASING OUR POTENTIAL OUTPUT

- Increasing Output (ACHIEVING OUR POTENTIAL), and

- Increasing Real GDP per capita

(1) INCREASING OUR POTENTIAL OUTPUT

This is increasing our ABILITY to produce. This is the

definition we used in the 5

Es lesson. This is the most fundamental definition of

economic growth. It is the type of economic growth used on our

5 Es diagram.

We can increase our ABILITY to produce goods and services

(or increase our POTENTIAL GDP) if we get:

- more resources

- better resources, and

- better technology

Since this increases maximum output that we are able to

produce it shifts the PPF outward. On the graph below, economic

growth would cause the PPF to move from PP1 to PP2.

This doesn't necessarily mean that the economy IS producing

more, just that it CAN produce more. To achieve our new

potential levels of output we also need full employment and

productive efficiency. It could be possible to have this type

of economic growth so that we CAN produce the quantities

represented by point E, but if there is unemployment and

productive inefficiency we would be at a point beneath this new

curve (maybe point C). So we may get new resources or new

technology so we CAN produce more (point E on PP2), but if we

don't use the new resources (i.e. we have unemployment) or if

we don't use the new technology (i.e. we have productive

inefficiency) , we may remain on PP1 (point C).

In the AS-AD model INCREASING OUR POTENTIAL OUTPUT is

represented by in increase in AS.

Notice that when AS increases, the full employment level of

output increase from RDO-FE1 to RDO-FE2. This is an increase in

our potential level of output.

In the 5 Es lecture we said that economic growth is caused

by:

- more resources

- better resources, or

- better technology

An increase in the production possibilities curve is caused

by having more resources, better resources, or better

technology.

An increase in AS is caused by:

- a decrease in the price of resources

- an increase in productivity

- lower business taxes and government red tape

These are all really the same thing.

(2) Increasing Output (or ACHIEVING OUR POTENTIAL)

The most commonly used definition of economic growth is simply

increasing output or producing more. (Later we will call this

INCREASING REAL GDP.) This is the type of economic growth most

often mentioned in news reports like http://money.cnn.com/2009/10/29/news/economy/gdp/index.htm

When an economy increases its output it is often said to have

achieved economic growth. But if by producing more we are simply

ACHIEVING OUR POTENTIAL, then we could also say that it is

REDUCING UNEMPLOYMENT or ACHIEVING PRODUCTIVE EFFICIENCY. On our

graph this would be represented by moving from point D to a point

on the curve (A, B, or C).

On our AD-AS model we could illustrate this type of growth

(producing more) by an increase in AD.

Notice that output increase from RDO-EQUIL to RDO', but the

full employment level of output, which is our potential level of

output, does not change (RDO-FE).

If AD increases enough so that the new equilibrium is at the

full employment level of output, it is analogous to going from a

point inside the production possibilities curve to a point on the

curve.

(3) Increasing Real GDP per capita

A third definition of economic growth is an increase in real

GDP per capita, or per person. We'll discuss this later.

Economic Growth: Three Definitions - REVIEW

1. Increasing our ABILITY to Produce (INCREASING OUR

POTENTIAL)

a. "economic growth" on the 5Es chart

b. shifting out to a new production possibilities curve

c. AS

d. causes:

(1) change in input prices (more resources)

(2) changes in the productivity of resource (better res.,

better tech.)

(3). legal-institutional environment

2. Increasing output or increasing Real GDP (ACHIEVING OUR

POTENTIAL)

a. achieving "full employment" and "productive

efficiency" (5Es)

b. going from a point inside the PPC to a point closer to the

PPC

c. AD

d. increasing GDP per capita

e. causes:

(1) producing at a minimum cost to achieve productive

efficiency

(a) not using more resources than necessary

(b) using resources where they are best suited

(c) Using the appropriate technology

(2) more spending to AD

and achieve full employment

(a) C

(b) I

(c) G

(d) Xn

3. GDP per capita:

real GDP at a faster rate than the increase in the population

Chapter 8 - Economic Growth

I am going to do things differently in this online lecture. Below

is a detailed outline of the textbook. You can use it to guide your

reading an for taking notes from the reading. I

will add my own notes.

I. Introduction

A. Learning objectives - After completing this chapter

the student should be able to:

- Define two measures of economic growth.

- Explain why growth is a desirable goal.

- Understand the institutional structure an economy needs if

it is to experience "modern economic growth" and ongoing

increases in standards of living.

- Identify two main sources of growth.

- Explain and apply the "rule of 70."

- Give average long-term growth rates for U.S. and

qualifications of raw data.

- Show economic growth using production possibilities

analysis and aggregate demand aggregate supply analysis.

- Describe the growth record of the U.S. economy since 1950,

including two measures of its long term growth rates.

- Identify six major factors that contributed to U.S.

economic growth according to empirical studies.

- List three primary reasons for productivity acceleration in

the United States since 1995.

- List five reasons for increasing returns during the period

of productivity acceleration.

- Evaluate the potential for the productivity acceleration to

be a permanent phenomenon.

- Identify and explain the arguments for and against economic

growth.

- Define and identify terms and concepts at the end of the

chapter.

II. Economic Growth.

A. Two definitions of economics growth are given.

1. The increase in real GDP, which occurs over a

period of time. Here the author does not

make a distinction between and increase in the potential GDP

and achieving the potential GDP. Both of these could cause an

"increase in real GDP.

2. The increase in real GDP per capita, which occurs over

time. This definition is superior if comparison of living

standards is desired. For example, China's 2003 GDP was $1410

billion compared to Denmark's $212 billion, but per capita

GDP's were $1110 and $33,750 respectively.

- Growth in real GDP does not guarantee growth in real GDP

per capita. If the growth in population exceeds the growth

in real GDP, real GDP per capita will fall.

B. Growth is an important economic goal because it means more

material abundance and ability to meet the economizing problem.

Growth lessens the burden of scarcity. That

is why we study it.

C. The arithmetic of growth is impressive. Using the "rule of

70," a growth rate of 2 percent annually would take 35 years for

GDP to double, but a growth rate of 4 percent annually would only

take about 18 years for GDP to double. (The "rule of 70" uses the

absolute value of a rate of change, divides it into 70, and the

result is the number of years it takes the underlying quantity to

double.)

- Note:

- small changes in the annual

percent growth of GDP results in large changes in GDP over

time

- know the "rule of 70"

D. Main sources of growth are increasing inputs or increasing

productivity of existing inputs.

1. About one-third of U.S. growth comes from more

inputs.

2. About two-thirds comes from increased productivity.

- Note:

- we said economic growth is cause

by:

- more resources

- better resources = greater

productivity

- better technology = greater

productivity

- here the authors are discussing an

INCREASE in POTENTIAL GDP

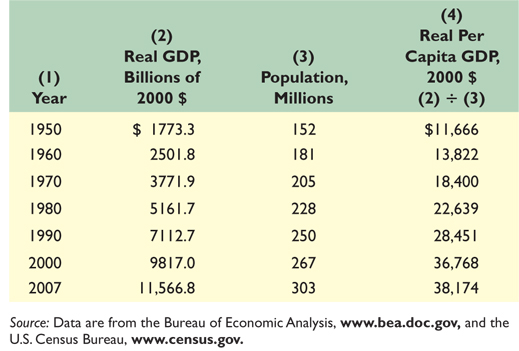

E. Growth Record of the United States (Table 8.1) is

impressive.

Table 8.1

1. Real GDP has increased over sixfold since 1950, and real per

capita GDP has risen over threefold. (See columns 2 and 4, Table

8.1)

2. Rate of growth record shows that real GDP has grown about

3.4 percent per year since 1950 and real GDP per capita has grown

about 2.1 percent per year. But the arithmetic needs to be

qualified.

III. Modern Economic Growth

A. Modern economic growth is characterized by sustained

ongoing increases in living standards that can cause dramatic

increases in the standard of living within a generation.

B. Economic historians informally date the start of the

Industrial Revolution to the year 1776, when Scottish inventor

James Watt perfected a powerful and efficient steam engine.

Note:

- there was little to no growth in

living standards from the beginning of time to about 200 years

ago

- during this period of little or no

growth all areas of the world had similar standards of

living

- therefore the type of economic growth

that we see now is a recent phenomenon in the history of the

world

- also, the great differences in living

standards is a recent phenomenon in the history of the

world

- How does "modern economic growth"

differ from what came before it?

C. The Uneven Distribution of Growth

1. Modern economic growth has spread only slowly from

its British birthplace. It first advanced to France, Germany,

and other parts of Western Europe in the early 1800's before

spreading to the Untied States, Canada, and Australia by the

mid 1800's.

2. The different starting dates for modern economic growth

in various parts of the world are the main cause of the vast

differences in per capita GDP levels seen today.

3. Figure 8.1 shows what economists have called the great

divergence in income levels around the world is a result of

different rates of, and starting dates for, modern economic

growth.

- What is the "great divergence"?

- According to the textbook, what is

the main cause for the "vast differences in in per capita

income levels seen today?

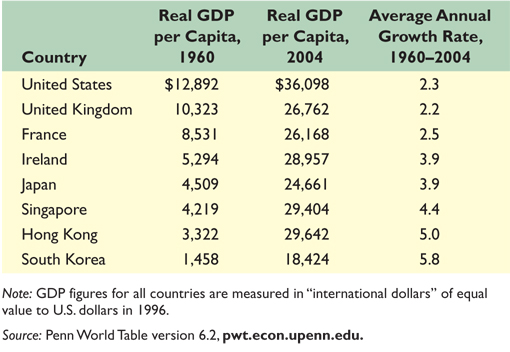

D. Catching Up is Possible

1. Countries that began modern economic growth more

recently are not doomed to be permanently poorer than the

countries that began modern economic growth at an earlier date.

2. The poorer 'follower countries' can grow much faster

because they can simply adopt existing technologies from rich

'leader countries'.

3. Table 8.2 shows both

- how the growth rates of leader countries are constrained

by the rate of technological progress

- is well is how certain follower countries have been able

to catch up by adopting more advanced technologies and

growing rapidly.

Table 8.2

- which countries are the "leader

countries" and which are the "follower

countries"?

- notice that the average growth

rates for the these follower countries is higher than for

the leader countries

- notice that with these growth rate

differences some follower countries have surpassed some

leader countries in real GDP per capita

- According to the authors, why is

the real GDP per capita of the United States in 2004 so much

higher than that of other rich countries?

4. CONSIDER THIS … Economic Growth Rates Matter

"Even small differences in

growth rates matter!"

IV. Institutional Structures That Promote Growth

A. Table 8.2 demonstrates that poorer follower countries

can catch up. But how does a country start that process?

B. Economic historians have identified several institutional

features that promote and sustain modern economic growth.

1. Strong Property Rights

2. Patents and copyrights (see the CONSIDER THIS …

Patents and Innovation)

b. Compounding makes seemingly small differences in

growth rates quite significant.

c. Over a 70-year period, a 4 percent growth rate will

generate twice is much output is a 3 percent growth rate,

and nearly four times is much income is a 2 percent growth

rate.

3. Efficient financial institutions

4. Literacy and widespread education

5. Free trade

6. A competitive market system

Note the role of Structural Adjustment

that we studied in unit 1:

- strong property rights -

privatization

- free trade

- a competitive market

system

The textbook lists some other

"difficult-to-measure" factors that help economic

growth:

- stable political

system

- internal order (no civil

wars)

- strong sense of the right of

property ownership

- strong legal status accorded to

businesses

- strong laws to enforce

contracts

- "no social or moral taboos on

production and material progress"

- belief that wealth creation is a

desirable goal

- positive attitude toward

work

- I would add that the more equal

status afforded to women in the leader countries has aided

economic growth

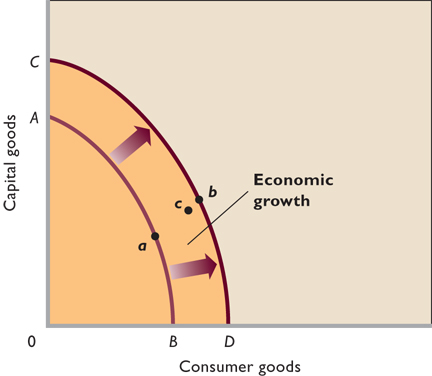

V. Ingredients of Growth

A. Four supply factors relate to the ability to grow.

[Shift the production possibilities

outward from AB to DC in Figure 8.2 below]

1. The quantity and quality of natural resources,

2. The quantity and quality of human resources,

3. The supply or stock of capital goods, and

4. Technology.

B. Two demand and efficiency factors are also related to

growth. [After the supply factors shift

the production possibilities the demand and productive efficiency

factors move the economy from a to c or b on the production

possibilities graph in Figure 8.2 below.]

1. Aggregate demand must increase for production to

expand.

2. Full employment of resources and both productive and

allocative efficiency are necessary to get the maximum amount

of production possible.

VI. Production Possibilities Analysis (Figure 8.2)

Figure 8.2

A. Growth can be illustrated with a production possibilities

curve (Figure 8.2), where growth is indicated is an outward shift

of the curve from AB to CD.

1. Aggregate demand must increase to sustain full

employment at each new level of production possible.

2. Additional resources that shift the curve outward must be

employed fully and efficiently (productive efficiency) to make

the maximum possible contribution to domestic output.

3. For the economy to achieve the maximum increase in value,

the optimal combination of goods must be achieved (allocative

efficiency).

Note: it may be useful to reread the

5Es lecture so that you are sure to know the difference between

productive efficiency and allocative efficiency.

[http://www.harpercollege.edu/mhealy/eco212i/lectures/ch1-18.htm]

VII. Accounting for growth is an attempt to quantify factors

contributing to economic growth.

A. More labor input is one source of growth. Labor force

has grown by 1.7 million workers per year for the past 52 years

and accounts for about one-third of total economic growth.

B. The growth of labor productivity contributed only about half

of the growth from 1973-1993, but was responsible for all it from

1995-2004, and is expected to account for about three-fourths of

the growth between 2005 and 2011.

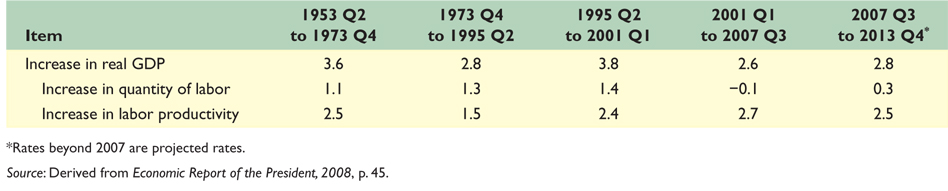

Table 8.3

Average annual percentage changes in the growth of real GDP

in the US and how much was the result of an increase in the

quantity of labor and how much was the result of an increase in

the productivity of labor

C. According to Table 8.3 between half and three quarters of

economic growth in the US during the past 50 -60 year is can be

explained by an increase in the productivity of labor (output per

worker), BUT WHAT CAUSED THE INCREASE IN PRODUCTIVITY?

Four causes of an increase in the productivity of labor:

1. Technological advance, the most important factor in

productivity growth, accounts for 40 percent of productivity

growth.

2. Increases in quantity of capital are estimated to explain

about 30 percent of productivity growth.

3. Education and training improve the quality of labor, and

account for about 15 percent of productivity growth. (See

Figure 8.4 below)

4. Improved resource allocation and economies of scale also

contribute to growth and explain about 15% of total

productivity growth.

a. Economies of scale occur is the size of markets and firms

that serve them have grown.

b. Improved resource allocation has occurred is

discrimination disappears and labor moves where it is most

productive, and is tariffs and other trade barriers are

lowered.

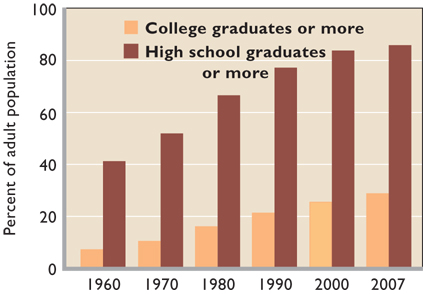

Figure 8.4 - Changes in the educational attainment of the

U.S. adult population

Note:

- the quantity of labor does NOT affect

the productivity of labor

- more workers would mean more

production

- but more workers does not necessarily

mean more productivity (more BETTER workers would increase

productivity)

- Know the difference between:

- production - the quantity that is

produced (the production of cars increased last

month)

- productive efficiency - producing

at the minimum cost (one of the 5Es)

- productivity - how much is

produced per unit of resources (output per worker per

hour)

- the quantity of labor affects

economic growth and the productivity of labor affects economic

growth, but just because we have more workers doesn't mean that

we have better workers

|

D. CONSIDER THIS … Women, the Labor Force, and

Economic Growth

1. The percentage of women working in the paid labor

force has risen from 40 percent in 1965 to 56 percent in

2006.

2. Women's productivity has increased with

greater investments in human capital. Productivity

increases have raised women's wages and increased the

opportunity cost of staying home.

3. Reduced birthrates, growth in industries

typically attracting women workers, urban migration,

increased availability of part-time jobs, and

antidiscrimination laws have all increased labor

market access for women.

4. in the US during the

recession of 2009 the number of women working

SURPASSED the number of men for the first time

http://www.nytimes.com/2009/02/06/business/worldbusiness/06iht-06women.19978672.html

- How do the restrictions

placed on the role of women in some countries

affect their rate of economic growth and their

living standards?

|

VIII. The Recent Productivity Acceleration

A. Improvement in standard of living is linked to labor

productivity - output per worker per hour

B. The U.S. is experiencing a resurgence of productivity growth

based on innovations in computers and communications, coupled

with global capitalism. Since 1995 productivity growth has

averaged 2.9% annually - up from 1.4% over 1973-95 period. The

"Rule of 70" projects real income will double in 24 years rather

than 50 years. (Figure 8.5).

Note: again the authors point

out the important role of structural adjustment when they say

"coupled with global capitalism"

Figure 8.5 Growth of labor productivity in the US,

1973-2007

C. Much of the recent improvement in productivity is due to

"new economy" factors such is:

Reasons for the Productivity Acceleration since the

mid-1990s:

1. Microchips and information technology are the basis

for improved productivity. Many new inventions are based on

microchip technology.

2. New firms and increasing returns characterize the new

economy.

a. Some of today's most successful firms didn't

exist 25 years ago: Dell, Compaq, Microsoft, Oracle, Cisco

Systems, America Online, Yahoo and Amazon.com are just a few

of many.

b. Economies of scale and increasing returns in new firms

encourage rapid growth.

Economies of scale mean

that is business get larger their average costs of

product (cost per unit produced) decreases. (The long run

aver total cost curve [from microeconomics] is

downward sloping

This means that they can produce

each unit of output with fewer resources

Graph showing economies of scale

over a wide rage of output

3. Sources of increasing returns and economies of scale

include:

a. More specialized inputs.

b. Ability to spread development costs over large output

quantities since marginal costs are low.

c. Simultaneous consumption by many customers at the same

time.

d. Network effects make widespread use of information

goods more valuable is more use the products.

e. Learning increases with practice.

- What is "simultaneous

consumption?

- What are "network

effects"?

- Note that simultaneous

consumption and network effects are relatively recent

phenomena

4. Global competition encourages innovation and

efficiency.

- another recent

phenomenon

D. Even if average growth rates in productivity and real output

growth remain higher over time, business cycle fluctuations (i.e.

recessions) can still occur. (like 2009)

E. Skepticism about long-term continued growth remains, and

only time will tell.

IX. Is Growth Desirable and Sustainable?

A. An antigrowth view exists. (Growth is bad)

1. Growth causes pollution, global warming, ozone

depletion, and other problems.

2. "More" is not always better if it means dead-end jobs,

burnout, and alienation from one's job.

3. High growth creates high stress.

B. Others argue in defense of growth. (Growth is good)

1. Growth leads to an improved standard of living.

2. Growth helps to reduce poverty in poor countries.

3. Growth has improved working conditions.

4. Growth allows more leisure and less alienation from

work.

5. Environmental concerns are important, but growth actually

has allowed more sensitivity to environmental concerns and the

ability to deal with them.

C. Is growth sustainable? Yes, say proponents of growth.

1. Resource prices are not rising.

2. Growth today has more to do with expansion and

application of knowledge and information, so is limited only by

human imagination.\]

Note: what about global climate

change?

X. LAST WORD: Economic Growth in China

A. China has been experiencing a period of remarkable

economic growth.

1. China's real output has grown over the past 25

years at a rate of nearly 9 percent per year, quadrupling real

output over that period.

2. Rising income has led to more saving, greater capital

investment, and more direct foreign investment, which has

helped fuel growth.

3. Per capita income has increased at an annual rate of 8

percent since 1980, despite China's population expanding by 14

million people per year.

4. Increased use of capital, better technology, labor

reallocation from agriculture, and increased privatization have

all contributed to greater productivity.

5. China's growth has been supported by a dramatic increase

in exports ($5 billion in 1978 to $1.2 trillion in 2007).

B. Despite its success, China faces a number of important

problems:

1. Inflation rates have been high at times (15 to 25

percent per year) because of too much spending relative to

capacity. Central banking reform has helped keep inflation low

in recent years.

2. State owned enterprises and banks operate unprofitably,

likely necessitating a government bailout.

3. China has a poor record of protecting intellectual

property rights, and keeps its currency artificially

undervalued. These issues have caused tension with the United

States and threaten to disrupt trade if they are not

resolved.

4. China's growth and development has been uneven, meaning

that there are many that have not benefited from the nation's

rising incomes.