Welcome to ECO 212

Macroeconomics in the Global Economy

|

http://www.youtube.com/watch?v=VVp8UGjECt4

Brief Outline:

- Introduction to ECO 212

- Why "Macroeconomics in the Global Economy"?

- The 5 E's of Economics

- Economic Growth

- Productive Efficiency

- Productive Efficiency

- Equity

- Full Employment

- What is MACROECONOMICS?

- Why Study Economics?

- The Use of Theories and Graphs in Economics

- Benefit Cost Analysis

- The Economizing Problem: Making Choices

- Limited Resources: The Four Factors of

Production

- Production Possibilities Frontier (Curve)

- Demonstrating the Necessity of Choice --

- Opportunity costs

- Law of Increasing Costs

- Unemployment

- Productive Inefficiency

- Economic Growth

- Present Choices and Future Possibilities

- International trade

- Marginal Analysis - How to make choices

1a Introduction to the Course

|

Introduction to ECO 212

Syllabus and Webpage:

- Mac Web App - put an icon on your mobile device

- roster

- Read the syllabus and take online syllabus quiz (5

points).

- Blackboard:

- Go to http://harper.blackboard.com

- Follow the instructions to "log-in",

- If you need help see the following on the Blackboard

opening page:

- "Getting Started with Blackboard"

- "Student Blackboard Technical Support"

- You should see our course listed under the "My Blackboard"

tab

- If you do not please e-mail the instructor:

mhealy@harpercollege.edu

- On Blackboard you will find:

COURSE INFO.

BEFORE CLASS

DURING CLASS

AFTER CLASS

FOR POINTS

OTHER

COURSE INFO.

- WELCOME EMAIL

- ANNOUNCEMENTS

- SYLLABUS

- SCHEDULE

- OFFICE HOURS

- FACULTY INFO.

BEFORE CLASS

- LESSONS

- PREQUIZZES

- VIDEO LOGIN

- MAC WEB APP

- Chapter 23W - 16th ed.

- Micro Ch. 16 - 19th ed.

- Ch. 22W, 19th ed.

DURING CLASS

- YELLOW PAGES

- LECTURE OUTLINES

- CLICKER QUIZZES

AFTER CLASS

- REQUIRED ACTIVITIES

- PRACTICE EXERCISES

- REVIEW QUIZZES

- FINAL EXAM REVIEW

- BUY STUDY GUIDE

- TEXTBOOK SOLUTIONS

- Answers to Key QuestionsThis link is hidden from

students

FOR POINTS

- SYLLABUS QUIZ

- PREQUIZZES

- REQUIRED ACTIVITIES

- PAPERS

- EXTRA CREDIT

OTHER

- ONLINE LECTURES

- DISCUSSION BOARD

- MY GRADES

- TEXTBOOK WEBSITE

- Option to Forward E-mail from your Harper Email Account

If you are not planning on using your Harper email account, you

can find instructions on how to forward email from that account to

one you check frequently by logging in to the Harper Student

Portal and clicking on the "My Harper E-Mail" tab. All

correspondence in this class will be sent to your Harper e-mail

account.

If you need further assistance, contact the Student Service

Desk at 847-925-6866, or email: studentsd@harpercollege.edu.

When e-mailing your instructor always put "ECO 212" and a

message in the subject line of all e-mails sent to the instructor.

Please use proper spelling, punctuation, and grammar.

- Syllabus :http://www.harpercollege.edu/mhealy/eco212/syllabus/macsylsi.htm

- Course Materials (This information is found on the

syllabus)

Brief list:

- Required Textbook: Macroeconomic by

Campbell R. McConnell, Brue, and Flynn, 19th edition,

McGraw-Hill, 2012 (Be sure to get the 19th

edition.)

- Required Online Videos: Tomlinson Videos on

Thinkwell

- Required Yellow Pages, (Free, distributed in class

and available on our Blackboard site)

- Mac Web App: An app for your cell phone or

tablet

- Recommended Textbook Study Guide: Study Guide

For Macroeconomics, McConnell/Brue/Walstad, 19th

edition, McGraw-Hill, 2012

REQUIRED:

|

TEXTBOOK: Macroeconomics by Campbell

R. McConnell, Brue, and Flynn, 19th edition, McGraw-Hill,

2012

Just the textbook. No textbook access codes. No

"Connect". NOTE: be sure to get the 19th

edition even though there is a 20th edition

available

|

REQUIRED:

|

Tomlinson Videos on ThinkWell

BUYING the Tomlinson Videos on ThinkWell

(Once you log in to the Thinkwell class site

click on the "Chapter Checklist" link for a list

of the videos by their number.)

- Go to: http://www.thinkwell.com

- Click on "Register" in the upper right corner

- In the "Classroom and Distance Learning" area use

the pull-down menu to select your state:

"Illinois"

- Use the pull-down menu to select your school:

"Harper College"

- Use the pull-down menu to select your class:

- Click on

- Then click on Checkout

to purchase for $49.

to purchase for $49.

- Follow the instructions to enter the required

fields.

- Next time you go to Thinkwell.com click on the

"Sign In" button to enter your username and

Password.

USING the Tomlinson Videos on Thinkwell:

- VIDEO

LOGIN is a link to sign into the Tomlinson video

lectures that you must purchase online. Assigned video

lectures are listed on the LESSONS

page with a numbering system that looks like: 1.1.1,

1.1-2, 2.1.1, etc.

- Once you log in to the Thinkwell class site

click on the "Chapter Checklist" link for a

list of the videos by their number.

- Note that each video can be watched FULL

SCREEN.

- Also, for each video you will have access to a

"Thinkwell Excercise" of from six to fifteen multiple

choice review questions, as well as Video Transcripts.

The exercises are quite useful.

Finally, you will want to have the VIDEO

NOTES handy when you are watching the videos

|

REQUIRED:

|

The Yellow Pages are packet of worksheets. We will do

many of the graphing exercises in class and some of the

Quick Quizzes. You will not get points for doing them,

but I think you will find them very useful while you

prepare for the quizzes and exams.

The Yellow Pages are available to you for free in

class or on our Blackboard site. Answers to the Yellow

Pages are also available on Blackboard. Make sure you

CHECK YOUR ANSWERS.

|

USEFUL:

|

MAC WEB APP:

The MacWebApp

has all of the information found on our LESSONS

page.

How to put an icon to the app on the homescreen of

your mobile device:

- On your cell phone or tablet go to the MacWebApp

home page (http://www.harpercollege.edu/mhealy/eco212/macwebapp/macwebapp.htm).

- Android: Launch Chrome for Android and open

the website or web page you want to pin to your home

screen. Tap the menu button and tap Add to homescreen.

You’ll be able to enter a name for the shortcut

and then Chrome will add it to your home screen.

- iPhone, iPad, & iPod Touch: Launch the

Safari browser on Apple’s iOS and navigate to the

website or web page you want to add to your home

screen. Tap the Share button on the browser’s

toolbar — that’s the rectangle with an arrow

pointing upward. It’s on the bar at the top of

the screen on an iPad, and on the bar at the bottom of

the screen on an iPhone or iPod Touch. Tap the Add to

Home Screen icon in the Share menu.

The app is not designed to replace your textbook,

computer, or paper and pencil. To learn the class

material you will have to read the textbook, watch the

Tomlinson video lectures, and DO PROBLEMS. When doing

problems you will need to use pencil and paper.

The app is designed to allow you to to do a

quick review after you have studied the

material.

The app is organized according our twenty-five

lessons. For each lesson you will usually find a quick

introduction, an interesting topic, the reading and video

assignments, key term flashcards, a quick review quiz,

key graphs, and YouTube review videos.

Be sure to put an icon to the app on your mobile

devices !!!

|

RECOMMENDED:

|

Study Guide For Macroeconomics,

McConnell/Brue/Walstad, 19th edition, McGraw-Hill,

2012

Printed:

- Can be bought online for less than

$20. Go to your favorite book site or search for:

ISBN 9780077337964

or

- The Study Guide can be bought at the Harper

College Bookstore (L building) or online at:

http://www.harperstore.com

- ISBN 9780077337964

- Cost about $65 new, $40 used, plus tax

Online:

- The Study Guide is also available in an online

version for only $15:

- To Purchase:

- Click on "I am a Student"

- Then, in the right column you can buy the

online version of the Study Guide by clicking on

- A USED PRINTED STUDY GUIDE can be bought

online for less than $15

|

OUTLINE -- CHAPTER 1

Limits, Alternatives, and Choices:

An introduction to Economics and the 5Es

I. Introduction to Macroeconomics in the Global Economy - Day

1

A. ACTIVITY:

|

QUESTION (use clickers):

Should the United States have free

trade with Mexico?

A. Yes

B. No

It Depends . . . .

- What GOAL are we trying to

achieve?

|

|

QUESTION (use clickers:

Assume that a hurricane has struck the

coast of Florida causing massive destruction. As a

result, the prices of many products like hotel

rooms, water, plywood, etc. increase significantly.

For example, let's say the price of plywood

increases from a price of $10 a sheet before the

hurricane to $30 a sheet after the hurricane.

What should the government do?

A. Pass a law to make these

"price-gouging" increases illegal returning the

price to $ 10

B. Nothing. Let the price of plywood rise

to $30 or more

C. Something else?

Again: What is the GOAL?

|

|

OTHER:

- Why the price of gasoline in the United States

is TOO LOW (we may have to wait until after we

finish chapter 5 to truly understand this.)

- Why it is GOOD when companies "outsource" (or

move) jobs to Japan and other countries (again, we

may not really understand this right away but we

should after chapter 20).

|

B. Why "the Global Economy"?

Welcome to ECO 212

Macroeconomics in the Global

Economy

|

1. Who has taken a MICROeconomics course (ECO

211)?

- no prerequisite

- need to review of microeconomic principles

- we'll do so, but in an international context

2. The three issues of Macroeconomics (ECO 212)

a. Unemployment (UE)

b. Inflation (IN)

c. Economic Growth (EG)

3. Global Economics is "in the news" BUT . . .

Dobbs: New Congress must show courage

[http://www.cnn.com/2006/US/11/28/Dobbs.Nov29/index.html]

Lou Dobbs, former CNN News commentator, says:

"We've lost three million manufacturing jobs as a result

of these so-called free trade agreements that enable

corporate America to export plants, production and jobs to

cheap foreign labor markets."

Then read the following quotes taken from our

textbook:

"The long-run impact of tariffs (restricting trade) is

not an increase in employment . . . (p. 489) "

" tariffs also reduce efficiency and the world's real

output" (p. 487)

4. Structural Adjustment and Globalization

C. Structural Adjustment - two examples

1. Microeconomic Example: Agriculture in China

http://www.npr.org/blogs/money/2012/01/20/145360447/the-secret-document-that-transformed-china

2. Macroeconomic Example - Video: Korea vs. Sri

Lanka

While watching the video look for answers to

these questions:

1. What are they doing? (POLICIES)

2. Why are they doing it? (BENEFITS)

3. What negative effects might arise? (COSTS)

|

To watch 5 minute video:

- Click on: http://www.learner.org/resources/series86.html

- Scroll down to:

- 10. Developing Countries - How these

nations have been helped or hurt by the rapid

growth since WWII. Case studies: comparing

South Korea and Sri Lanka; aid vs. trade in

Tanzania.

- Click on

(A free

registration may be required)

(A free

registration may be required)

- Then slide the timer to minute 7:45 for the

eight minute South Korea vs. Sri Lanka case

study

|

- Cuba Examines Asian Model For Economic

Reforms (NPR Morning Edition)

|

3. News Articles:

- Some people oppose Structural Adjustment / Free

Trade

- But most economists, political leaders and people (?)

support SAPs

D. Why?

- Why are countries all over the world undertaking

Structural Adjustment Programs (SAPs)?

- To answer this we need to:

- Understand the GOAL of Economics

- Learn the 5 Es of Economics

- Learn some fundamental economic

principles

- That is what we will be doing in unit 1

- Cuba Examines Asian Model For Economic

Reforms (NPR Morning Edition)

|

II. Short Introduction to Structural Adjustment

Programs

A. Introduction

B. Economic Systems

C. Structural Adjustment Policies

VIDEO: Poland

- Privatization

- Promotion of Competition

- Reduced Role of Government

- Removing Price Controls

- Freer Trade and Convertible Currency

- Foreign Investment

- Other

|

Available online at:

- Click on: http://www.learner.org/resources/series86.html

- Scroll down to:

- 11. Economies in Transition: Transforming

former Communist countries into market

economies. Case studies: state industries vs.

private entrepreneurs in Russia; the success of

Poland’s “shock therapy.”

- Click on

(A free

registration is required for first time

users)

- Then slide the timer to minute 27:25 for the

eight minute the success of Poland’s

“shock therapy case study

|

D. Goals of SAPs

- Maximize society's satisfaction = improve the

standard of living

- Macroeconomic Goals:

- full employment

- low inflation

- economic growth

E. Problems with SAPs:

- initial inflation and unemployment

- initial falling output and living standards

- inequality and social costs - some people are worse

off

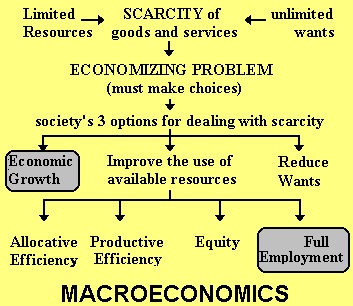

1b The 5Es of Economics (or How to Reduce Scarcity)

|

REVIEW: Why Globalization? Listen How

Are People In Europe Reacting To Trump's Rhetoric?

[NPR Morning Edition, Jan. 23, 2017, 5:47]

PREVIEW:

- Why the price of gasoline in the United States is TOO LOW

(we may have to wait until after we finish chapter 5 to truly

understand this.)

III. The Economic Perspective: Scarcity and

Choice -- the 5Es of Economics

A. Scarcity -- Limited resources and Unlimited

wants

- The reason why we have to make

choices

- economic definitions are sometimes different - define

"scarcity"

- "erskinite"

B. Unlimited Wants and the necessity of choice

C. Solving the Economizing Problem: Options for Dealing with

Scarcity

1. economic growth ( the first "E")

2. reducing wants

3. use existing resources wisely = maximizing satisfaction

1. economic growth ( the first "E")

a. DEFINITION: an increase in the ABILITY to

produce goods and services

[This is NOT the same as the common definition: an

increase in output]

b. caused by:

- MORE resources

- better resources

- better technology

c. textbook:

"An

outward shift in the production possibilities curve which

results from an increase in resource quantity or quality or

an improvement in technology"

(more on this later)

d. Economic growth is one of the three issues of

Macroeconomics --We'll discuss economic growth in more

detail later in this chapter, in unit 2, and throughout the

semester.

2. reducing wants

3. use existing resources wisely = maximizing

satisfaction

IV. Maximizing Satisfaction -- Four More

Es

- Maximizing satisfaction from EXISTING resources

- The goal of SAPs

[StrucAdjDef]

- 5Es

A. Productive Efficiency

B. Allocative Efficiency

- 1. definition

2. How does this MAXIMIZE SOCIETY'S SATISFACTION and

REDUCE SCARCITY?

3. examples

- a. steel: horseshoes or cars

b. crude oil: gasoline or kerosene

c. small cars or SUVs

4. Allocative inefficiency

5. The role of prices in achieving allocative

efficiency

C. Equity

D. Full Employment

|

F. Review

1. What is Structural

Adjustment?

2. Why are they doing

it?

a. What is

Economics?

b. What is the

GOAL?

c. What are the

5Es?

d. How does EACH of the 5Es

reduce scarcity and achieve this

goal?

3. Compare market economies and

command economies as to how well they achieve the

5Es.

|

Lesson 1c: Making Choices: Production Possibilities

Curve (PPC) and Benefit Cost Analysis

|

V. What Is Economics?

A. Need to know basic economic principles to

understand WHY the world is moving toward Structural Adjustment or

Globalization

B. DEFINITION:

1. MARK'S

DEFINITION OF ECONOMICS:

2. TEXTBOOK'S DEFINITION : Economics is the social

science concerned with how individuals, institutions, and

society make optimal (best) choices under conditions of

scarcity.

- What I like: The emphasis on making

CHOICES

- What is unclear: What does "SCARCITY" mean?

- GOAL OF ECONOMICS: BEST CHOICES = Maximize

Satisfaction !

3. OUR DEFINITION: Economics is the social science

that studies how we choose to use limited

resources to obtain the maximum satisfaction of

unlimited human wants

C. The definition has 4 parts:

- social science

- choice

- scarcity

- maximizing satisfaction

VI. "Social Science" -- Using theories

A. based on facts

B. simplifications

C. generalizations

D. abstractions

E. ceteris paribus

VII. Why Study Economics

VIII. Limited Resources: The Four Factors of

Production

A. What is a resource?

B. Types of Resources

1. Land

a. examples

b. definition

2. Capital

a. examples

b. definition

3. Labor

a. examples

b. definition

4. Entrepreneurial Ability

a. examples

b. definition

C. Resource

Quiz (yellow page)

D. Resources and Resource Payments

1. land -- rent

2. capital -- interest

3. labor -- wages

4. entrepreneurial ability -- profits or losses

IX. Economic Models

A. Demonstrating economic concepts

B. Line Graphs

1. construction

2. inverse and direct relationships

3. slope

a. linear (straight) graph

b. nonlinear (bent) graph

X. MAKING CHOICES - WHY? - The

Necessity of Choice -- Production Possibilities

A. Society's Economizing Problem -- The

Necessity of Choice

The

choices necessitated because society’s material wants for

goods and services are unlimited but the resources available to

satisfy these wants are limited.

1. Unlimited Wants

2. Limited resources

B. Production Possibilities -- Demonstrating the Necessity

of Choice

|

The Production Possibilities Curve can be use to

illustrate several important economic

concepts:

- we must make choices

- choices have opportunity costs

- the law of increasing costs

- the effect of unemployment

- the effect of productive

inefficiency

- the effect of economic growth

- how present choices affect future

possibilities

- it does NOT show the optimum product mix

(allocative efficiency)

|

1. Production

Possibilities Table

a. shows the MAXIMUM POSSIBLE LEVELS OF

PRODUCTION given the assumptions

b. assumptions

- fixed resources

- fixed technology

- productive efficiency

- full employment

- only two goods

3) the necessity of choice -- Unattainable

combinations

2. Production Possibilities Curve

a. the necessity of choice -- Unattainable

combinations

b. opportunity costs

1) ALL costs in economics are opportunity

costs

2) definition

The

amount of other products which must be forgone or

sacrificed to produce a unit of a product.

3) examples

- op. cost of coming to class today

- op. cost of attending NIU

- op. cost of a free trip to Europe

- What is the op. cost of a human life?

4) calculating opportunity costs

c. law of increasing costs

1) definition

As

the production of a good increases the opportunity

cost of producing an additional unit rises.

2) shape of the PPC -- concave

3) rationale

d. unemployment

e. productive inefficiency

f. economic growth (Macro Issue)

1) Two (Three) Definitions

- Increasing our ABILITY to Produce = INCREASING

OUR POTENTIAL (Ch. 1 / 5Es Def.)

- Increasing Output = ACHIEVING OUR POTENTIAL

(Ch. 8 Def. ?)

- graphically

- reduce UE

- reduce. prod ineff.

- GDP per capita (Ch. 8 Def.)

2) a

shrinking PPC?

3) non-proportional growth

g. present choices, future possibilities

h. optimum product mix? (allocative efficiency?)

C. Real World Applications of the

PPC

1. The economics of War (p. 14)

- defense good, civilian goods and the "war on

terror"

- Marginal Benefit and Marginal Costs

- 9/11 increase the MB of defense goods

2. discrimination

3. growth: Japan vs. U.S.

4. international trade

XI. MAKING CHOICES - HOW? - The Necessity of

Choice -- Benefit Cost Analysis: How to make choices

p. 5, Fast Food Lines (box)

p. 5, "Marginal Analysis: Benefits and Costs"

pp. 13-14, "Optimal Allocation" (especially fig 1.3),

p. 14 "The Economics of War" (box)

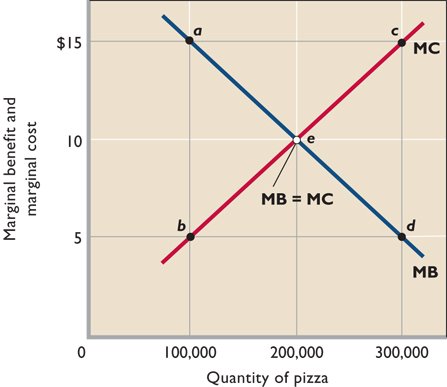

A. Benefit-Cost Analysis

"the economic perspective")

1. definition

the selection of ALL possible alternatives where

the marginal benefits are greater than the marginal cost

select all where: MB > MC

up to where: MB = MC

but never where: MB < MC

TEXTBOOK: Marginal Analysis:

the comparison of marginal ("extra" or "additional")

benefits and marginal costs, usually for decision making

.

2. marginal benefits and marginal costs

marginal benefit

The extra (additional)

benefit of consuming one more unit of some good or service;

the change in total benefit when one more unit is

consumed.

marginal

cost

The extra (additional) cost

of producing one more unit of output; equal to the change in

total cost divided by the change in output (and in the short

run to the change in total variable cost divided by the

change in output).

3. Marginal

Benefit = Marginal Cost Rule

- The point

at which the size or scope of production (or any decision)

is optimized.

- The

activity, scope, or output of a project (or decision) should

be increased until it reaches this point - or comes very

close to it.

- This point

will yield the maximum net benefit to society.

- If marginal

benefit exceeds marginal cost, then the project is too

modest, and could be increased thereby increasing the net

benefit to society;

- however, if

the marginal cost exceeds the marginal benefit, then the

project will decrease the net benefit to society and should

be decreased in scope.

- For

example, if the cost of a proposed government program

exceeds its benefits, then it would be unwise to undertake

it, but if the benefits exceed the cost, then it would be

uneconomical, or "wasteful" not to spend on that government

program.

4. ignore fixed or sunk costs

a fixed or sunk cost is any cost that does not

change as a result of the decision

TEXTBOOK: A fixed cost is

any cost which in total does not change when the firm

changes its output; the cost of fixed resources.

5. examples

a. How many guards should be hired?

b. How many bridges should be built?

c. Should I go to class today?

d. should I attend NIU full time?

e. Should I drive fast?

f. The economics of War (p. 14)

defense good, civilian goods and the "war on

terror"

Marginal Benefit and Marginal Costs

9/11 increase the MB of defense goods

g. Sunk costs are irrelevant in decision

making

- buy tickets to football game but wake up with the

flu - should you go?

- you buy "mushy" apples, should you eat

them?

- already paid a nonrefundable annual lease for a

business - should you move to a more profitable

location

- $1 million spent on R&D for a new product that

few people want - should you produce it anyway even at a

loss?

- Pfizer's insulin inhaler

- New Coke

- McLean

- you already bought the ring - should you therefore

marry him/her?

e.Others

Think of a decision that you currently have

to make. What are the marginal benefits and the marginal

costs? Are there any sunk costs that do not matter?

6. GRAPHICALLY

7. REVIEW

a. End-of-chapter questions Chapter 1, #9

Specify and explain the typical shapes of the

marginal-benefit and marginal-cost curves. How are these

curves used to determine the optimal allocation of

resources to a particular product. If current output is

such that marginal cost exceeds marginal benefit, should

more or fewer resources be allocated to this product?

Explain.

ANSWER: The marginal benefit curve is downward

sloping, MB falls as more of a product is consumed

because additional units of a good yield less

satisfaction than previous units. The marginal cost curve

is upward sloping, MC increases as more of a product is

produced since additional units require the use of

increasingly unsuitable resource. The optimal amount of a

particular product occurs where MB equals MC. If MC

exceeds MB, fewer resources should be allocated to this

use. The resources are more valuable in some alternative

use (as reflected in the higher MC) than in this use (as

reflected in the lower MB).

b. Multiple Choice

Problems

|

The following data are for a series of

increasingly extensive flood control

projects:

|

|

|

|

|

Total cost

per year

|

MC

|

Total benefit

per year

|

MB

|

|

No project

|

|

|

$ 0

|

------------

|

$ 0

|

------------

|

|

Plan A

|

levees

|

10,000

|

|

|

20,000

|

|

|

|

Plan B

|

small reservoir

|

24,000

|

|

|

34,000

|

|

|

|

Plan C

|

medium reservoir

|

44,000

|

|

|

42,000

|

|

|

|

Plan D

|

large reservoir

|

72,000

|

|

|

40,000

|

|

|

|

1. Refer to the above data. For Plan D marginal costs

and marginal benefits are:

A. $72,000 and $64,000 respectively.

B. $28,000 and $2,000 respectively.

C. $24,000 and $18,000 respectively.

D. $16,000 and $28,000 respectively.

2. Refer to the above data. On the basis of

benefit-cost (marginal) analysis government should:

A. undertake Plan A.

B. undertake Plan B.

C. undertake Plan C.

D. undertake Plan D.

3. Plan C above entails:

A. marginal benefits in excess of marginal

costs.

B. fewer spillovers than either Plan A or Plan

B.

C. an overallocation (too much) of resources to

flood control

D. an underallocation (too little) of resources to

flood control.

See answers below

ANSWERS:

|

|

|

|

|

Total cost

per year

|

MC

|

Total benefit

per year

|

MB

|

|

No project

|

|

|

$ 0

|

--

|

$ 0

|

--

|

|

Plan A

|

levees

|

10,000

|

10,000

|

20,000

|

20,000

|

|

Plan B

|

small reservoir

|

24,000

|

14,000

|

34,000

|

14,000

|

|

Plan C

|

medium reservoir

|

44,000

|

20,000

|

42,000

|

8,000

|

|

Plan D

|

large reservoir

|

72,000

|

28,000

|

40,000

|

2,000

|

1. For Plan D marginal costs and marginal benefits

are:

B. $28,000 and $2,000 respectively.

Be sure that you can calculate MB and MC.

If you need help ask on the Discussion

Board

2. Refer to the above data. On the basis of

benefit-cost (marginal) analysis government should:

B. undertake Plan B.

Do all options as long as the MB are

greater then the MC (MB>MC)

3. Plan C above entails:

C. an overallocation (too much) of resources

to flood control

For plan C the MB are less than the MC

(MB<MC). this means tat too many resources are

being used on these flood control projects. To say

this another way, IF the MB are less than the MC it

means that you have other uses for these resources

that will give you more benefits. Remember, the MC

of any decision is the benefits of other

alternatives that you are not doing.

XII. The Circular Flow Model

A. The flow

of resources from households to firms and of products from firms

to households. These flows are accompanied by reverse flows of

money from firms to households and from households to

firms.

1. Two Markets

a. product market

A market

in which products are sold by firms and bought by

households.

1) how much to buy

2) how much to produce

b. resource market

A market

in which households sell and firms buy resources or the

services of resources.

1) how many to hire

2) how much we earn

2. Two Flows

a. real flow

b. money flow

3. Reversal of Roles

4. Limitations

B. The Circulr Flow Diagram

{kind=link}