ECO 211 Microeconomics: An

Introduction to Economic Efficiency

|

- Contact

Information and Office Hours

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 1a: The Class and the

Math

Welcome to ECO 211! My name is Mark Healy. I will

be your economics instructor for the semester. Please call me

"Mark".

Many students end up dropping or failing this

course due to the lack of basic math skills. If your math skills are

weak you should consider building them before taking this course. If

you are required to take MTH 060 or MTH 082 and have not yet done so,

do not take this economics course until you have successfully

completed one of them. The face-to-face sections will take a practice

math quiz on the first day of class. For the online section I have

posted the math quiz on our Blackboard site. Take the math quiz on

Blackboard or in class. If you score less than 14 or 15, consider

dropping ECO 211 and taking a math class first.

1a Something Interesting - Why are we

studying this?

|

Optional: a funny look at some major ideas

of economics by the "Stand-up Economist".

Principles

of economics, translated

(5:20)

Ch.1, Appendix on Graphing

Syllabus

On-Campus / Syllabus

Online

Start: 5Es

online reading

Lecture

Outline

1a Assignments: Video

Lectures

|

REVIEW OF GRAPHING CONCEPTS

1.2.1 Using

Graphs to Understand Direct Relationships

9:50 [MyNotes]

1.2.2

Plotting

A Linear Relationship Between Two Variables

9:57 [MyNotes]

1.2.3

Changing

the Intercept of a Linear Function

8:42 [MyNotes]

1.2.4

Understanding

the Slope of a Linear Function 7:28

[MyNotes]

OPTIONAL:

Khan Academy Exercise:

Graphing

Points

Khan

Academy Exercise: Graphing

Points 2

OPTIONAL:

MATH, ALGEBRA, AND GEOMETRY FOR ECONOMICS STUDENTS

How

to Multiply and Divide Fractions in Algebra for

Dummies (YouTube fordummies

1:50)

Simple

Equations (Khan Academy

11:06)

Solving

One-Step Equations (Khan Academy

1:54)

Solving

One-Step Equations 2 (Khan Academy

2:23)

Practice

(Khan Academy )

Solving

Ax + B = C (Khan Academy

8:41)

Area

and Perimeter (Khan Academy

12:20)

1a Outcomes - What you should

learn

|

how to find class information

- syllabus

- Blackboard

- Yellow Pages

- SCHEDULE

- LESSONS webpage

- MICWEBAPP

- Key term Flashcards

- WebQuizzes

basic math skills

- calculate marginal

- calculate average

- arithmetic of fractions and

decimals

- find area of a rectangle

- find area of a triangle

- basic algebra

- calculate and use percentages

- graph a line on a Cartesian coordinate

system

- marginal is the slope of the

total

Key Terms

Flash Cards - Click Here

The Class:

Required Activity, Yellow Pages,

Tomlinson Videos on Thinkwell, Video Notes, LESSONS webpage,

Pre-quiz, Clicker Quiz, Web Quiz, Practice Exercises,

The Math:

horizontal (x) axis, vertical (y)

axis, origin, direct (positive) relationship, inverse (negative)

relationship, slope of a line, positive slope, negative slope,

marginal, average

Slope = rise/run

Slope = vertical change / horizontal change

Slope = marginal value of the total

Marginal = change in total / change in

quantity

The area under a marginal curve = the

total

Average = total / quantity

Total = average x quantity

Total = the sum of the marginal

Any Point on a Graph Represents Two

Numbers

Direct Relationship

Inverse Relationship

Calculating Slope

The area under a marginal curve = the

total

Episode

5A: Models & Theories

[3:26 YouTube mjmfoodie]

Episode

6: Graph Review

[4:22 YouTube mjmfoodie]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 1b: The 5Es of

Economics

The "5Es of Economics" are not from the textbook.

I borrowed the concept (with many modifications) from another

textbook many years ago. I believe it concisely explains the purpose

of economics. Also, it begins to introduce students to the economic

way of thinking. The economic problem that we all face, that all

countries face, that the world faces, is SCARCITY. Economics is the

study of how we can reduce scarcity. What I like about the 5Es model

is that it shows us that there are only five ways to reduce scarcity.

Only five. I call them the "5Es" of economics.

For each of the 5Es:

(1) learn the definition,

(2) understand examples, and

(3) most importantly, know how they reduce scarcity and help to

increase society's satisfaction.

This is where you learn that it may be good

when the price of plywood increases greatly as the result of a

hurricane. And why it might be good when Coca-Cola lays of one fifth

of its workforce. Or, that the price of gasoline may be too low.

Really!

1b Something Interesting - Why are we

studying this?

|

When a hurricane hits the coast of Florida,

prices of many necessities like food, water, hotel rooms, gasoline,

and even plywood, tend to increase. Some governments try to prevent

such price increases and call them "price-gouging".

See: http://www.csmonitor.com/1992/0910/10083.html

But economists think that such price increases

are GOOD for the people ravaged by the hurricane. WHY? Why is it GOOD

when the prices of products (like plywood) increase during a natural

disaster?

See: https://www.masterresource.org/price-gouging-law/defense-price-gouging/

ANSWER: Allocative Efficiency

5Es

online reading (VERY

IMPORTANT!)

Ch. 3: "Efficient Allocation" pp.

58-59

Ch. 3 and 6: "Diminishing Marginal Utility" pp.

49 and 117

Lecture

Outline

1b Assignments: Video

Lectures

|

Episode

5A: Models & Theories

[3:26 YouTube mjmfoodie]

1b Outcomes - What you should

learn

|

TOPICS:

- Introduction to Economics

- The 5Es of Economics

OUTCOMES:

Key

Terms Flash Cards - Click Here

Key Terms:

5Es, scarcity, economic growth,

allocative efficiency, productive efficiency, equity, full

employment, marginal, law of diminishing marginal utility,

President Trump example

The 5Es of Economics

Scarcity

and Exchange- EconMovies #1: Star Wars

[6:39 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 1c: Scarcity and Budget

Lines

So, do you agree that it is GOOD for the people

of Florida if, after a hurricane strikes, the price of plywood (or

other products) increases from $10 a sheet to $30 a sheet? Or, that

it was GOOD when the Coca-Cola company (or other companies) layed off

6000 workers as they did in the year 2000 assuming that they could

still produce the same quantity, but with fewer workers? Even if you

do not agree, do you understand that these things will reduce

scarcity and increase society's satisfaction? In chapter 5 we will

learn why the prices of products like gasoline, soda pop, and junk

food, may be TOO LOW. (Isn't this fun?)

Lesson 1c introduces our first graphic MODEL:

the budget line. For many students microeconomics is a difficult

course. I think there are two reasons for this. First, we will learn

theories or models, rather than facts. Facts are easy to memorize.

Theories or models have to be learned and practiced. And second, we

will express our theories or models on graphs, and many students do

not like graphs. If you want to be successful in this course you must

learn to use our graphical models. You must be able to draw the

graphs correctly from memory, you must understand what each line on

the graph represents, and you must know why each line has the shape

that it does. For each graph be able to: DEFINE, DRAW, DESCRIBE its

shape. Be sure to study the graphs in the textbook carefully and plot

all the graphs in the yellow pages. Finally, an easier way to view

graphs is to remember that each point on a graph represents two

numbers. Find a point on a graph, then find the two number from the

graph's axes.

Note: not all models are graphs. For example,

the 5Es of Economics is a model of the issues studied by

economists.

1c Something Interesting - Why are we

studying this?

|

USING MODELS: In this lesson we will learn our

first MODEL - the budget line. We will study many MODELS this semster

and most models will be represented by graphs. Why do economists use

so many models?

Read the first paragraph only ("About

this course:", Click on "More") of the link below. It introduces a

MOOC from the University of Michigan called "Model Thinking". I was a

bit surprised that there is a whole couse just on using models, but

it highlights the importance of models in understanding the world

around us.

https://www.coursera.org/learn/model-thinking

OPTIONAL - More information about the

importance of using models:

http://www.utexas.edu/courses/bio301d/Topics/Models/Text.html

http://www.imf.org/external/pubs/ft/fandd/basics/models.htm

Ch 1, pp. 1-11

Lecture

Outline

1c Assignments: Video

Lectures

|

WHAT IS ECONOMICS: SCARCITY, THE 5Es, AND MAKING

CHOICES

1.1.1 Scarcity

- Defining Economics 6:35

[MyNotes]

1.1.2

What

Economists Do 13:20

[

Summary] [Quiz]

[MyNotes]

1.1.3

Macroeconomics

and Microeconomics 11:21

[MyNotes]

EconMovies-

Episode 2: Monty Python and the Holy Grail - Marginal

Analysis (YouTube ACDCLeadership)

5:27

BUDGET

LINES

3.2.1 Constructing

a Consumer's Budget Constraint 9:36

[MyNotes]

3.2.2

Understanding

a Change in the Budget Constraint 5:02

[MyNotes]

1c Outcomes - What you should

learn

|

TOPICS

- Definition of economics

- Economic models (Why do economists use all

those graphs?)

- Budget lines

- Resources (Four Factors of Production)

OUTCOMES

- Define economics and describe the four

components of the definition:

- social science

- choice

- scarcity

- maximizing satisfaction

- What are economic models and why do

economists use them?

- Explain the importance of ceteris

paribus in formulating economic principles.

- Differentiate between microeconomics and

macroeconomics.

- Defne and draw budget lines. Explain what

happens to a budget line when income and prices

change.

- How does the budget line illustrate the

necessity of making choices?

- Define and give examples of the four types

of resources (factors of production) and know the payment for

each

Key Terms

Flash Cards - Click Here

Key Terms:

economics, economic model,

microeconomics, macroeconomics, utility, rational choice,

opportunity cost, benefit-cost analysis (marginal analysis),

ceteris paribus (other things equal assumption), budget line,

budget constraint, factors of production, resource, land, labor,

capital, entrepreneurial ability

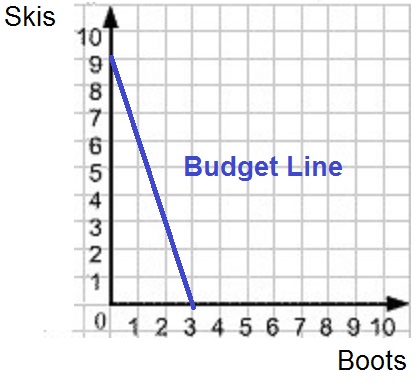

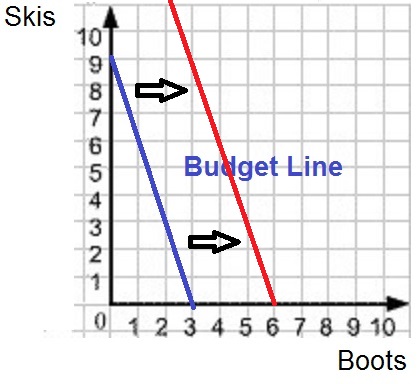

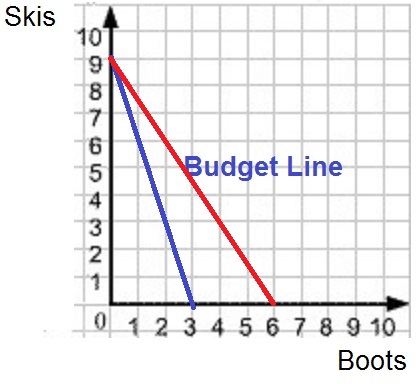

Budget Line

Budget Line: Income Increases

Budget Line: Price Decreases

Scarcity

and Exchange- EconMovies #1: Star Wars

[6:39 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

1d Making Choices: Production

Possibilities Curve (PPC) and Benefit Cost Analysis

(BCA)

Here we will study our second graphical model:

the Production Possibilities Curve (PPC), and we then will learn a

tool for making decisions that we will use throughout the course:

Benefit-Cost Analysis (BCA). Basically what we are doing is setting

the stage for making economic decisions. Remember: economics is the

social science concerned with how we CHOOSE to use our limited

resources to maximize society's unlimited wants, or, how we make

decisions.

The production possibilities curve will show us

that we must make choices and all choices have costs. Economists call

these "opportunity costs". ALL COSTS IN ECONOMICS ARE OPPORTUNITY

COSTS. Whenever we discuss the "costs" of doing something we will

mean the complete opportunity cost.

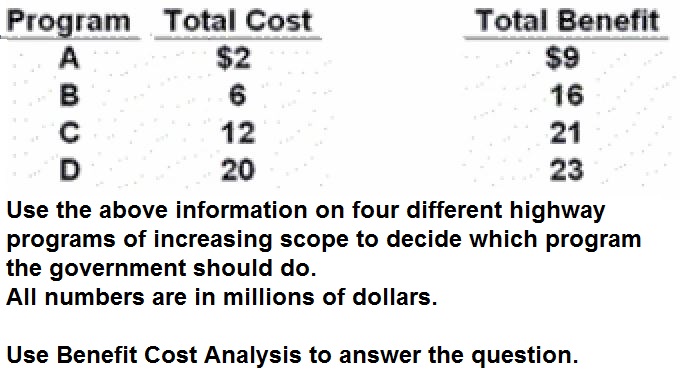

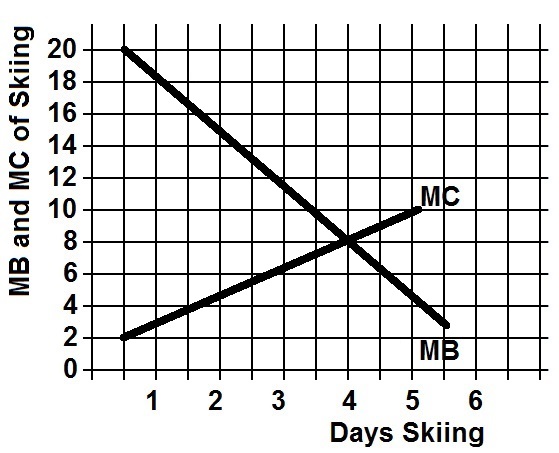

Benefit-cost analysis (BCA) is a model that

explains how to make the best decision possible. BCA means we should

select all options where the marginal benefits (MB) are greater than

the marginal costs (MC) -- up to where MB = MC. When the MB = MC then

we have made the best decision possible. NOTE: "marginal" means

"extra" or "additional". So to make the best decision possible select

all options where the extra benefits that you get from the decision

are greater than the extra costs of the decision. One more thing: to

make the best decisions we look only at MARGINAL costs and benefits

and we ignore FIXED, or SUNK, costs (i.e. ignore things that will not

change no matter what choice is made).

We will use BCA many times throughout this

course. In chapter 6 we will use BCA to decide how much to buy to

maximize our satisfaction. In chapters 8-11 we will use it to decide

how much to produce to maximize profits. In chapters 12 and 13 we use

BCA to decide how many to hire to maximize profits (Ch. 12 and

13).

Notice that economists look at EXTRA benefits

and EXTRA costs. We call this "thinking on the margin". Students are

used to thinking about TOTAL benefits and TOTAL costs. We do not want

total benefits to equal total costs, but we do want MB to equal MC.

You probably know that it is best if the total benefits are a lot

higher than total costs. What you will learn is that when MB = MC,

then the difference between total benefits and total costs will be

the greatest.

Be sure you understand BCA!

What is the connection between the PPC and BCA?

Well, when studying the PPC you will learn the important concept of

"opportunity cost". Learn the definition well. Since all costs in

economics are opportunity costs, then when using BCA, "marginal

costs" mean the additional opportunity costs.

1d Something Interesting - Why are we

studying this?

|

The link below discusses a study that concludes

that drivers of cars with air bags have more accidents. Why would

airbags in cars cause more accidents (see the link below)?

After studying this lesson you should be able

to use Benefit-Cost Analysis (MB=MC) to answer this question. When

airbags were first put in cars how did that change the extra benefits

of driving fast (MB) and the extra costs of driving fast (MC)?

Drivers

with airbags may take more risks

A similar question for skiers is why did the

invention of avalanche airbags cause more people to become caught in

avalanches (see below)? After studying this lesson you should be

able to use Benefit-Cost Analysis (MB=MC) to answer this

question.

In a March

2013 blog post written by Utah

Avalanche Center Director Bruce Tremper . . . Tremper says airbags

are providing a false sense of security, leading more skiers into

high-consequence terrain, and thus decreasing the effectiveness of

said airbag.

"Each gizmo we buy to increase our

safety usually cause us to increase our level of risk at the

same time. For instance, when we added seat belts and airbags

to cars, yes fatalities decreased, but it also allowed us to

drive faster, farther, crazier and talk on our mobile phones at

the same time. So safety measures usually work but not nearly

as well as we would hope because people just increase their

risk (and “utility”) at the same time. In avalanche

airbag case, we will also get more powder, more fun, and more

risk in the bargain . . . . people will increase their exposure

to risk because of the perception of increased safety, which

will cancel out some, but not all, of the effectiveness of

avalanche airbag."

What are avalanche airbags?

https://www.youtube.com/watch?v=h7QFRXc0R8M

Ch 1: Production Possibilities Model, pp.

11-21

Ch. 1: p. 5, "Marginal Analysis: Benefits and

Costs"

Ch. 1: pp. 13-14, "Optimal Allocation"

(especially Fig 1.3),

Drivers

with airbags may take more risks

Ch 1: p. 14, "The Economics of War"

(box)

Lecture

Outline

1d Assignments: Video

Lectures

|

PRODUCTION POSSIBILITIES

1.4.1 Understanding

the Concept of Production Possibilities

Frontiers 24:46

[MyNotes]

1.4.2

Understanding

How a Change in Technology Affects the PPF

10:10 [MyNotes]

ECONMOVIES

Episode 3: Monsters Inc. and the Production Possibilities

Curve

MAKING

CHOICES: THE ECONOMIC WAY OF THINKING -- BENEFIT-COST ANALYSIS (also

called Marginal Analysis or Cost-Benefit Analysis)

EconMovies-

Episode 2: Monty Python and the Holy Grail - Marginal

Analysis (YouTube ACDCLeadership

5:27)

Thinking

at the Margin (YouTube LearnLiberty

4:32)

Incentives

and Marginal Analysis (YouTube

MrHurdleHistory 8:54)

CIRCULAR

FLOW MODEL

Micro

1.1 The BIG Picture- AP Economics Overview (with links to

playlists) (YouTube ACDCLeadership

12:49)

10.1.2 The

Circular Flow Model 9:38

[MyNotes]

1d Outcomes - What you should

learn

|

TOPICS

- Society's Economizing Problem: Production

Possibilities

- How to Make Choices: Benefit-Cost

Analysis

OUTCOMES

Production Possibilities

Benefit Cost Analysis

- define benefit cost analysis (BCA) and use

it to solve problems

- define "marginal" and give

examples

- define marginal benefits (MB) and marginal

costs (MC)

- explain why we ignore fixed, or sunk, costs

("Don't cry over spilt milk.")

- know what happens if MC increase?

decrease?

- know what happens if MB increase?

decrease?

- draw MB and MC on a graph and explain their

shapes

- be able to find the optimum choice from a

table of total costs and total benefits and from a table of

marginal costs and marginal benefits

- use BCA to explain why Drivers

with airbags may take more risks or

why skiers

with air bags may take more risks

- what is a "sunk cost" (or fixed cost) and

why are they ignored when using benefit-cost analysis?

- "Don't cry over spilt milk " If you are

deciding whether or not to come to class today, why does it not

matter that you have already paid tuition? Why is the fact that

you have paid tuition irrelevant when trying to decide whether to

attend class today or skip?

Key Terms

Flash Cards - Click Here

Key Terms:

PPC:

production possibilities, necessity of choice, law of increasing

costs, concave to the origin, opportunity cost, constant cost,

benefit-cost analysis (marginal analysis), economic growth,

consumer goods, capital goods, shrinking PPC, nonproportional

growth

BCA:

marginal costs (MC), marginal benefits (MB), MB=MC Rule, sunk

(fixed) costs

Using

Benefit Cost Analysis (BCA)

Benefit Cost Analysis (BCA)

1d Key Graphs

|

|

The Production Possibilities Curve

(PPC)

PPC: Unemployment to Full

Employment and Productive

Inefficiency to Efficient

PPC and Economic Growth

Benefit Cost Analysis

|

- Production

Possibilities Curve- Econ 1.1

[3:56 YouTube ACDC Leadership]

- Shifting

the Production Possibilities Curve (PPC)- Econ

1.2

[5:35 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 2a: Market Economies and

Trade

One reason why I use our textbook is because they

have a chapter on market economies and they used to have a chapter on

command economies (now just a small section). In this lesson we find

out for the first time that competitive market economies are

efficient, both allocatively and productively. This is the result of

the "invisible hand" of capitalism. This is a general theme for the

whole course that we will discuss again in chapters 3, 5, and 8-13.

Many textbooks simply assume that students know what a capitalist

economy (market economy) is because we live in one here in the United

States. But, I learned long ago that students do not understand the

characteristics of captialism nor the benefits of, or the problems

with, market economies. All over the world countries are moving away

from command economies toward a market economy. Why? We will learn it

is because market economies are better at achieving allocative and

productive efficiency, and economic growth, but they do seem have a

problem with equity and at times full employment.

One characteristic of a market economy is a

limited role for governement. Periodically we will discuss just WHAT

IS the economic role of government? What should the government do, or

not do? This is where Republicans and Democrats seem to have a

fundamental disagreement, but I think they agree more than they

believe. Remember this: the economic goal of society is to maximize

its satisfaction (reduce scarcity as much as possible). And they do

this by achieving the 5Es. The economic role of government then ALSO

should be to achieve the 5Es. We will return to this issue of the

economic role of government at different times thoughout the

course.

Our first discussion of this economic role for

government will be FREE TRADE. Should the United States have free

trade with other countries like Mexico and China, or should the

government impose trade restrictions? We will examine this question

by using the production possibilities model that we learned in

chapter 1.

2a Something Interesting - Why are we

studying this?

|

Read the first four paragraphs of

The

Mystical Power of Free Trade.

After studying this lesson you should

understand:

- why "society benefits from allowing

its citizens to buy what they wish--even from foreigners." (i.e.

free trade helps society),

- and why "people resist this conclusion,

sometimes violently"

Ch. 2 ALL

pp. 474-482

A

Comparison of Market Economics and Command Economies

Lecture

Outline

2a Assignments: Video

Lectures

|

ECONOMIC SYSTEMS

1.1.4 An

Overview of Economic Systems 10:50

[MyNotes]

Power

of the Market (YouTube LibertyPen)

1:14 [MyNotes]

17.5.3

Comparative

Economic Performance 12:16

[MyNotes]

OPTIONAL:

Paul

Solman Video: Capitalism vs. Socialism - The Cuban

Quandary (YouTube PBS NewsHour)

13:56

SPECIALIZATION

AND GAINS FROM TRADE

1.5.1 Defining

Comparative Advantage with the Production Possibilities

Frontier 22:10 [MyNotes]

1.5.2

Understanding

Why Specialization Increases Total Output

6:46 [MyNotes]

1.5.3 Analyzing

International Trade Using Comparative

Advantage 25:35

[MyNotes]

KEY PROBLEM: The

gains from trade

2a Outcomes - What you should

learn

|

TOPICS

- How Countries Make Economic Choices:

Economic Systems

- Market Economies

- Command Economies

- Capitalism and the Five Fundamental

Questions

- Capitalism and Efficiency (the invisible

hand)

- The Gains from Trade

OUTCOMES

- Pure Laissez-faire economic

system

- Centrally Planned Economy

- mixed economic systems

- The Bolshevik Revolution

- Contributing factors to the collapse of the

Soviet Union

- characteristics of the market

system

- the important role of profits and

losses

- property rights

- the "invisible hand" of

capitalism

- the coordination problem

- the incentive problem

- be able to draw and explain the Circular

Flow Model

- Why are market economies more efficient

than command economies both allocatively and

productively?

- What is the "invisible hand" of

capitalism

- How does trade increase productive

efficiency and therefore output?

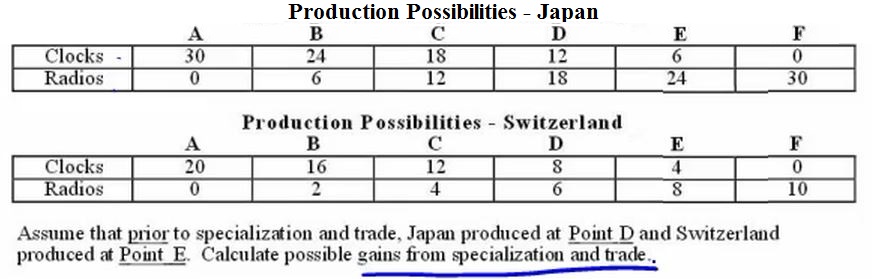

- calculate how specialization and trade

increases output using the production possiblilities tables and

graphs of two different countries

- straight line PPCs (constant

costs)

- absolute advantage

- comparative advantage

- calculate comparative

advantage

- specialization and trade

- calculate the gains from specialization

and trade

Key Terms

Flash Cards - Click Here

Key Terms:

economic system, command system (centrally

planned, socialism), market system (capitalism, laissez-faire), mixed

economic system, Bolshevik revolution, self interest, private

property, freedom of enterprise and choice, competition, market,

specialization, consumer sovereignty, dollar votes, invisible hand,

creative destruction, coordination problem, incentive problem,

circular flow diagram, product market, resource market, opportunity

cost, absolute advantage, comparative advantage, gains from trade,

free trade.

The

Gains from Trade

Click on the link above to learn how to do this

problem.

Comparative Advantage and the Gains from

Trade

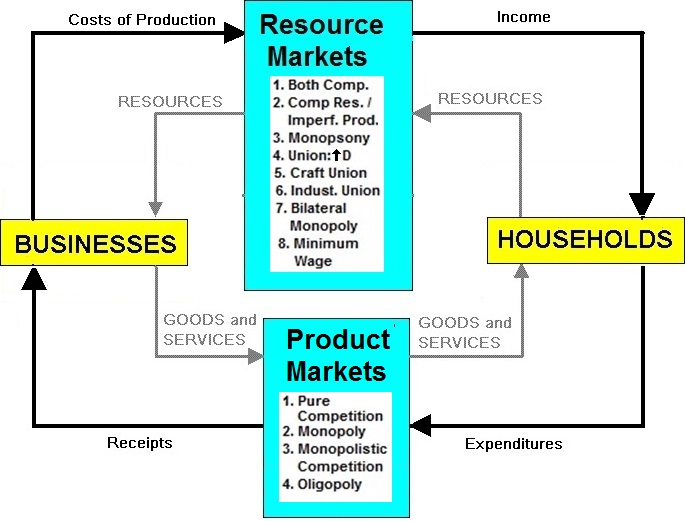

Circular Flow Model of Capitalism

- Econ

1.6- Economic Systems: Why is Communist China doing so

well?

[4:13 YouTube ACDC

Leadership]

- Comparative

advantage specialization and gains from trade | Microeconomics | Khan

Academy

[8:55 YouTube Khan Academy]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for thise assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 3a: Demand

If the price of pizza goes up, what happens to

the demand for pizza? . . . . . . . . . . . . . . . . . . . NOTHING!

Nothing happens to the demand for pizza if the price

changes!

The next three lessons introduce the demand and

supply model for explaining how prices arise and change in a market

economy. Learn these lessons well. Do the assigned problems. Draw the

graphs in the yellow pages and while you are reading and studying.

DRAW GRAPHS! Get used to using the graphs to help you answer

questions. If you are avoiding drawing the graphs you will do poorly

and not get the practice that you need to learn the concept. Be sure

to LABEL the axes of every graph that you draw.

So why doesn't the demand for pizza change if

the price changes? Because economists have a different definition of

"demand". Demand is NOT the quantity that we buy. If the price of

pizza goes up we will buy less, but that is not what "demand" means

in economics. Economists tend to be precise with their definitions

and sometimes their definitions are different than the more commonly

used definitions. Things like "scarcity", "investment", "cost",

"demand", and "supply", have different definitions in economics than

what you may already know. Learn our definitions! Demand is not how

much we buy. Demand has a different definition in economics. "Demand"

means the "demand graph".

Remember, that econmists use models (like the

supply and demand model) to simplify the real world. They do this by

isolating certain variables from all the clutter found in reality.

Then by changing one variable at a time economists can see what

effect it will have. In this lesson we will learn the economic

definition of DEMAND and plot the demand graph. Then, we will look at

one variable at a time to see what effect they have on the demand

curve. We call these variables the "non-price determinants of

demand". They are: Pe, Pog, I, Npot, T (P,P,I,N,T). LEARN THEM! LEARN

THEM WELL! Know how each one affects the demand curve. Be sure to do

the yellow pages.

3a Something Interesting - Why are we

studying this?

|

What is that Campbell's Pork and Beans can doing

on the display for VanCamp's Pork and Beans (see below)?

After studying this lesson you will be able to

draw a graph illustrating what happened to the demand for

Campbell's Pork and Beans when a customer took a can out of their

shopping cart and placed it on this display of VanCamp's Pork and

Beans that were on sale.

Which non-price determinant of demand explains

why that Campbell's soup can is there?

Ch 3, pp. 47-53

Optional,

but very useful

Lecture

Outline

3a Assignments: Video

Lectures

|

2.1.1 Understanding

the Determinants of Demand 11:58

[MyNotes]

2.1.2

Understanding

the Basics of Demand 11:54

[MyNotes]

2.1.3

Analyzing

Shifts in the Demand Curve 8:13

[MyNotes]

2.1.4

Changing

Other Demand Variables 10:43

[MyNotes]

2.1.5

Deriving

a Market Demand Curve 9:16

[MyNotes]

OPTIONAL:

The

Law of Demand (econclassroom.com

11:24)

Changes

in Demand versus Changes in Quantity

Demanded (econclassroom.com

5:52)

The

Determinants of Demand

(econclassroom.com 11:07)

3a Outcomes - What you should

learn

|

TOPICS

- Definition of demand

- Changes in Demand vs. Changes in Quantity

Demanded

- Non-price determinants of demand and how

they affect the demand curve

OUTCOMES

- define demand (note: it has a

DIFFERENT DEFINITION in economics)

- If the price of pizza goes up, why does the

demand for pizza stay the same?

- be able to correctly draw and label a

demand graph

- why do economists employ the ceteris

paribus assumption when creating a demand curve?

- what is the law of demand?

- why is the demand curve downward sloping

(three explanations)

- list the non-price determinants of demand

(Pe. Pog, I, Npot, T) or (P, P, I, N, T ) and understand how they

affect the demand schedule and curve. This is VERY IMPORTANT. BE

ABLE TO DO THIS! See the 3a/3b/3c yellow pages.

- explain the difference between the a

"change in the quantity demanded" and a "change in

demand"

- what is an "increase in demand" and a

"decrease in demand" and show how they affect the demand schedule

and the demand curve

- what is "market demand"?

- what is that Campbell's Pork and Beans can

doing on the display for VanCamp's Pork and Beans (see picture at

left)? Which non-price determinant of demand explains why that

Campbell's soup can is there? Draw a supply and demand graph

illustrating what happened in the market for Campbell's Pork and

Beans when VanCamp's were put on sale.

3a Non-Price Determinants of Demand

and Supply

|

Non-Price Determinants of Demand (PPINT)

Pe -- expected price

Pog -- price of other goods

1) substitute goods

2) complementary goods

3) independent goods

I -- income

1) normal goods

2) inferior goods

N -- number of POTENTIAL consumers

T -- tastes and preferences

Non-Price Determinants of Supply

(PPPTTN)

Pe -- expected price

Pog -- price of other goods produced by same firm

Pres -- price of resources

T --technology

T --taxes and subsidies

N -- number of producers/sellers

NON-PRICE DETERMINANTS OF DEMAND

Pe -- expected price

Pe

in the future

Pe

in the future  D today

D today

Pe in the future

D today

Pe in the future

D today

Pog -- price of other goods

1) substitute goods

P Maxwell House coffee

D Folgers coffee

P of one product

D of its substitute

2) complementary goods

P of wieners

D of buns

P of one product

D of its compliment

I -- income

1) normal goods

Income

D for normal goods

Income

D for normal goods

2) inferior goods

Income

D for inferior goods

Income

D for inferior goods

Npot -- number of POTENTIAL

consumers

Npot

D

Npot

D

T -- tastes and preferences

Tastes for a product

D for that product

Tastes for a product

D for that product

NON-PRICE DETERMINANTS OF SUPPLY

Pe -- expected price

Pe in the future

S today

Pe in the future

S today

Pog -- price of other goods also produced by

the same firm

P soybeans

S corn

P soybeans

S corn

Pres -- price of resources

worker's wages

cost of making cars

S cars

Pres

costs

S

Pres

costs

S

Tech --technology

Improved technology

costs

S

Tax --taxes and subsidies

Taxes

costs

S

Taxes

costs

S

Subsidies

costs

S

Subsidies

costs

S

N -- number of

producers/sellers

Nproducers

S

Nproducers

S

Key Terms

Flash Cards - Click Here

Key Terms:

demand, quantity demanded, law of

demand, market demand, horizontal summation, income effect,

substitution effect, diminishing marginal utility, change in

demand, change in quantity demanded, increase in demand, decrease

in demand, non-price determinants of demand, normal good, inferior

good, substitute good, complementary good (complement),

independent goods

The Demand Curve

Changes in Demand

Increase in Demand

Decrease in Demand

Market Demand (horizontal summation of

individual demand curves)

- Demand

and Supply Explained- Econ 2.1

[6:20 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 3b: Supply

If the price of pizza goes up what happens to the

SUPPLY of pizza? . . . . . . . . . . NOTHING!

A change in the price of a product does not

affect its supply, or its demand. When the price goes up the QUANTITY

SUPPLIED will increase, but the supply does not change. Learn the

difference between "supply" and "quantity supplied". "Supply" does

NOT MEAN the quantity available for sale. Supply has a different

definition in economics. "Supply" means the "Supply

graph".

So what would cause the supply graph, or supply

itself, to change? Those things that cause supply to change are

called the "non-price determinants of supply". They are: Pe, Pog,

Pres, Tech, Tax, Nprod (P,P,P,T,T,N). See the Yellow

Pages.

Remember, the goal of chapter 3 is to learn a

model that will help us understand why prices are what they are and

why prices change. In the next lesson we will put demand and supply

together and use the model (graph) to find the prices of products.

Then, and more importantly, we will see what causes prices to change.

If you hear on the news, or read in your news app, that the price of

gasoline is going down, we will be able to explain WHY. The causes of

changes in prices of products are the five non-price determinants of

demand (Pe, Pog, I, Npot, T) and/or the six non-price determinants of

supply (Pe, Pog, Pres, Tech, Tax, Nprod.). Whenever you hear that the

price of something is changing think of these 11 possible

causes.

3b Something Interesting - Why are we

studying this?

|

Read the short news article below on the

declining price of gasoline (Dec. 2015). Paragraph 10 states

"Plunging oil prices are the main factor driving down the price at

the pump."

Gas

falls below $2 a gallon [http://money.cnn.com/2015/12/20/news/economy/aaa-2-dollar-gas/index.html]

After studying this lesson you should be able

to:

(1) list the non-price determinants of

supply

(2) select the determinant that is the cause of the decline in

gasoline prices discussed in the news article, and

(3) graph the effect that the change in the determinant will have on

the supply curve for gasoline.

Ch. 3, pp. 53-56

http://www.npr.org/blogs/parallels/2015/01/28/382173205/where-is-all-that-excess-oil-going

[Why are they storing oil? What is happening to supply? Which

determinant has caused the supply to change?]

Optional,

but very useful

Lecture

Outline

3b Assignments: Video

Lectures

|

2.2.1 Understanding

the Determinants of Supply 7:25

[MyNotes]

2.2.2

Deriving

a Supply Curve 9:49

[MyNotes]

2.2.3

Understanding

a Change in Supply versus a Change in Quantity

Supplied 6:52 [MyNotes]

2.2.4

Analyzing

Changes in Other Supply Variables 8:47

[MyNotes]

2.2.5 Deriving

a Market Supply Curve from Individual Supply

Curves 7:16 [MyNotes]

3b Outcomes - What you should

learn

|

TOPICS

- Definition of supply

- Changes in Supply vs. Changes in Quantity

Supplied

- Non-price determinants of supply and how

they affect the supply curve

OUTCOMES

- define supply (note: it has a DIFFERENT

DEFINITION in economics)

- be able to correctly draw and label a

supply graph

- if the price of pizza goes up why does the

supply not change?

- why do economists employ the ceteris

paribus assumption when creating a supply curve?

- what is the law of supply?

- why is the supply curve upward sloping (two

explanations)

- list the non-price determinants of supply

(Pe, Pog, Pres, Tech, Taxes, Nprod) or (P,P,P,T,T,N) and

understand how they affect the supply schedule and curve. This is

VERY IMPORTANT. BE ABLE TO DO THIS! See the 3a/3b/3c yellow

pages.

- explain the difference between the a

"change in the quantity supplied" and a "change in

supply"

- what is an increase in supply and a

decrease in supply and show how they affect the supply schedule

and the supply curve

- what is "market supply"?

- Read the following and answer these

questions:

- Which determinant has

changed?

- Will it affect S or D of

gasoline?

- Will the S or D of gasoline increase or

decrease? Shift to the right or to the left?

"According to the Lundberg Survey, the

average price for regular gasoline dropped 3.99 cents over the

three weeks up to July 11 to $3.6699 per gallon. . . . Lundberg

explained that the average gasoline price continues to decrease

because refiners, enjoying the lower crude oil prices in the

market, are passing down the savings to the consumers.

"

From: http://www.techtimes.com/articles/10378/20140714/average-price-of-gasoline-in-u-s-drops-four-cents-now-at-3-67-a-gallon.htm

3b Non-Price Determinants of Demand

and Supply

|

Non-Price Determinants of Demand (PPINT)

Pe -- expected price

Pog -- price of other goods

1) substitute goods

2) complementary goods

3) independent goods

I -- income

1) normal goods

2) inferior goods

N -- number of POTENTIAL consumers

T -- tastes and preferences

Non-Price Determinants of Supply

(PPPTTN)

Pe -- expected price

Pog -- price of other goods produced by same firm

Pres -- price of resources

T --technology

T --taxes and subsidies

N -- number of producers/sellers

NON-PRICE DETERMINANTS OF DEMAND

Pe -- expected price

Pe

in the future

D today

Pe in the future

D today

Pog -- price of other goods

1) substitute goods

P Maxwell House coffee

D Folgers coffee

P of one product

D of its substitute

2) complementary goods

P of wieners

D of buns

P of one product

D of its compliment

I -- income

1) normal goods

Income

D for normal goods

Income

D for normal goods

2) inferior goods

Income

D for inferior goods

Income

D for inferior goods

Npot -- number of POTENTIAL

consumers

Npot

D

Npot

D

T -- tastes and preferences

Tastes for a product

D for that product

Tastes for a product

D for that product

NON-PRICE DETERMINANTS OF SUPPLY

Pe -- expected price

Pe in the future

S today

Pe in the future

S today

Pog -- price of other goods also produced by

the same firm

P soybeans

S corn

P soybeans

S corn

Pres -- price of resources

worker's wages

cost of making cars

S cars

Pres

costs

S

Pres

costs

S

Tech --technology

Improved technology

costs

S

Tax --taxes and subsidies

Taxes

costs

S

Taxes

costs

S

Subsidies

costs

S

Subsidies

costs

S

N -- number of

producers/sellers

Nproducers

S

Nproducers

S

Key Terms

Flash Cards - Click Here

Key Terms:

supply, quantity supplied, market

supply, law of supply, change in supply, change in quantity

supplied, increase in supply, decrease in supply, non-price

determinants of supply

The Supply Curve

Changes in Supply

Increase in Supply

Decrease in Supply

- Demand

and Supply Explained (2 of 2) - Econ 2.2

[4:54 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 3c: Market Equilibrium and

Efficiency

We are going to learn two very important things

in this lesson.

First, we will put demand and supply together

and learn how to use the model to to see why products have the prices

that they do. Then, and more importantly, we will see what causes

prices to change.

If you hear on the news or read in your news

app, that the price of gasoline is going down, we will be able to

explain WHY. The causes of changes in prices of products are the five

non-price determinants of demand (Pe, Pog, I, Npot, T) and/or the six

non-price determinants of supply (Pe, Pog, Pres, Tech, Tax, Nprod.).

Whenever you hear that the price of something is changing think of

which of these 11 possible causes have changed, draw the graph and

shift the appropriate demand and/or supply graph, and the graph will

show the price changing.

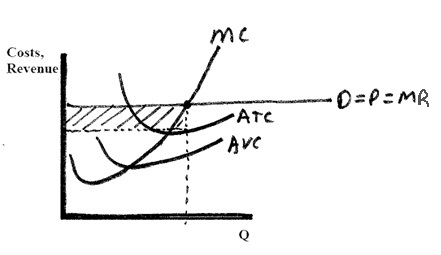

Second, after we learn that in a competitive

market economy the interaction of demand and supply will determine

what the prices of products will be and how much people will buy at

that price, we will ask: Is this the allocatively efficient quantity

and price? Our goal is to show that in a competitive market the price

will change until allocative efficiency is achieved. In chapter 2 we

learned that competitive markets are allocatively efficient. This

means they will produce the quantity of goods that maximizes the

society's satisfaction. After studying chapter 3 we will be able to

show the allocatively efficient price and quantity on a

graph.

Competitive markets are efficient.

3c Something Interesting - Why are we

studying this?

|

Read the first few paragraphs of Hybrid

Car Prices Increasing Due To High Gas Prices.

In lesson 3a you learned how the non-price

determinants of demand (Pe, Pog, I, N, T) affect the demand curve.

In lesson 3b you learned how the non-price

determinants of supply (Pe, Pog, Pres, Tech, Tax, Nprod) affect the

supply curve.

After studying this lesson you will be able to

use these determinants and the supply and demand graphs to explain

why prices change.

For example you will understand why: "It's

becoming almost an annual tradition: As fuel prices rise in the

spring, so do the prices of hybrid cars. "

Ch. 3 pp. 56-61, 69-74

Ch. 5: pp. 93-99, Efficiently Functioning

Markets

Supply,

Demand, and Economic Efficiency

Optional,

but very useful

Lecture

Outline

3c Assignments: Video

Lectures

|

PUTTING SUPPLY AND DEMAND TOGETHER

2.3.1 Determining

a Competitive Equilibrium 11:04

[MyNotes]

2.3.2

Defining

Comparative Statics 7:02

[MyNotes]

2.3.3

Classifying

Comparative Statics 11:54

[MyNotes]

AC

Micro

2.4 Double Shifts in Supply and Demand: Econ Concepts in 60

Seconds (2:34)

EconMovies:

Episode

4: Indiana Jones (Demand, Supply, Equilibrium,

Shifts) (7:02)

MARKETS AND

EFFICIENCY

Consumer

and Producer Surplus in the Linear Demand and Supply

Model (econclassroom.com

10:01)

Efficiency

and Equilibrium in Competitive Markets

(econclassroom.com 11:48)

3c Outcomes - What you should

learn

|

TOPICS

- Market Equilibrium

- Market Equilibrium and Changes in D and

S

- Market Equilibrium and Allocative

Efficiency

- MSB=MSC

- maximum consumer plus producer

surplus

OUTCOMES

Equilibrium

- what are the two assumptions of a

competitive equilibrium?

- there are many buyers and sellers in the

market

- who have no influence over the price;

i.e. they are price takers

- define equilibrium; define market

equilibrium

- what happens if the price is below the

equilibrium price? If it is above it?

- how to find the equilibrium price and

quantity on a supply and demand schedule and graph

- define "shortage" and "surplus" and explain

using a supply and demand graph

- what is the "bidding

mechanism"?

- the three (or four) steps to finding a new

equilibrium when a non-price determinant changes and how to use

them

- what happens to the equilibrium price and

quantity if (1) demand increases, (2) demand decreases, (3) supply

increases, and (4) supply decreases.

- what happens if both supply and demand

change

Markets and Efficiency

- be able to use two models to show why

competitive market economies achieve allocative efficiency

- MSB=MSC

- maximum consumer plus producer

surplus

- define marginal social benefit and explain

why it is often measured by the demand curve

- define marginal social cost and explain why

it is often measured by the supply curve

- explain why allocative inefficiency occurs

where MSB > MSC causing an underallocation of resources (too

little produced); show on graph using the MSB=MSC

model

- explain why allocative inefficiency occurs

where MSB < MSC causing an overallocation of resources (too

much produced); show on graph using the MSB=MSC model

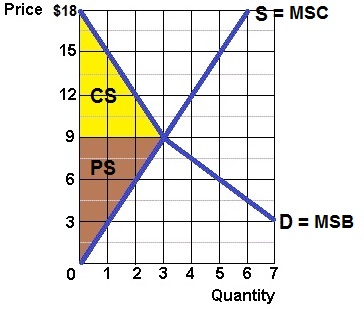

- be able to find WHAT WE GET and WHAT WE

WANT on the MSB=MSC model graph

- define consumer surplus and producer

surplus and shade them in on a supply and demand graph

- define deadweight loss and be able to

locate it on a supply and demand graph if too much or too little

is produced

3c Non-Price Determinants of Demand

and Supply

|

Non-Price Determinants of Demand (PPINT)

Pe -- expected price

Pog -- price of other goods

1) substitute goods

2) complementary goods

3) independent goods

I -- income

1) normal goods

2) inferior goods

N -- number of POTENTIAL consumers

T -- tastes and preferences

Non-Price Determinants of Supply

(PPPTTN)

Pe -- expected price

Pog -- price of other goods produced by same firm

Pres -- price of resources

T --technology

T --taxes and subsidies

N -- number of producers/sellers

NON-PRICE DETERMINANTS OF DEMAND

Pe -- expected price

Pe

in the future

D today

Pe in the future

D today

Pog -- price of other goods

1) substitute goods

P Maxwell House coffee

D Folgers coffee

P of one product

D of its substitute

2) complementary goods

P of wieners

D of buns

P of one product

D of its compliment

I -- income

1) normal goods

Income

D for normal goods

Income

D for normal goods

2) inferior goods

Income

D for inferior goods

Income

D for inferior goods

Npot -- number of POTENTIAL

consumers

Npot

D

Npot

D

T -- tastes and preferences

Tastes for a product

D for that product

Tastes for a product

D for that product

NON-PRICE DETERMINANTS OF SUPPLY

Pe -- expected price

Pe in the future

S today

Pe in the future

S today

Pog -- price of other goods also produced by

the same firm

P soybeans

S corn

P soybeans

S corn

Pres -- price of resources

worker's wages

cost of making cars

S cars

Pres

costs

S

Pres

costs

S

Tech --technology

Improved technology

costs

S

Tax --taxes and subsidies

Taxes

costs

S

Taxes

costs

S

Subsidies

costs

S

Subsidies

costs

S

N -- number of

producers/sellers

Nproducers

S

Nproducers

S

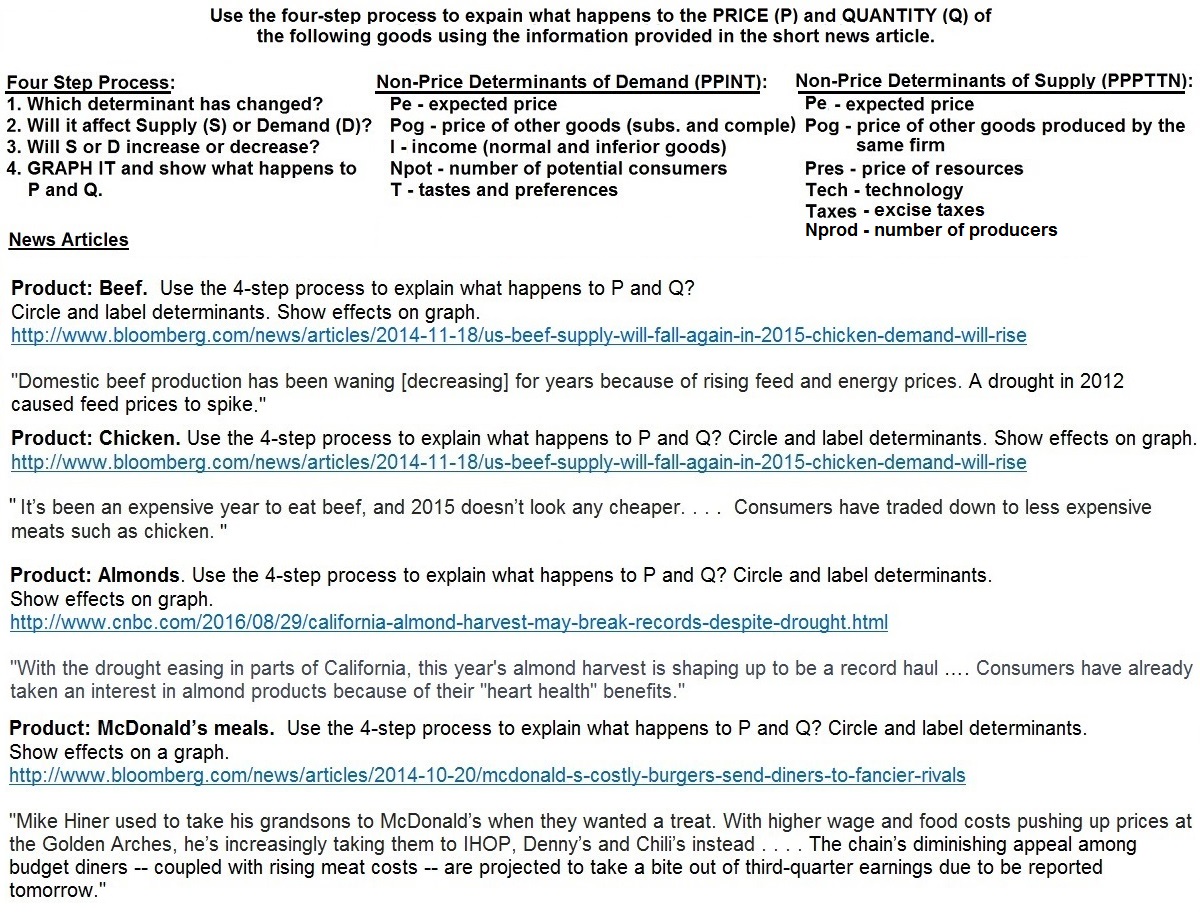

Beef

and Chicken

Almonds

McDonald's

Click on the links above to learn how to use a

supply and demand graph to show why prices and quantities change. The

exam 1 extra credit questions will be similar to these

problems.

Key Terms

Flashcards - Click Here

Market Equilibrium

equilibrium, market equilibrium,

bidding mechanism, surplus, shortage, scalping,

Efficiency

productive efficiency, allocative

efficiency, marginal social benefits, marginal social costs, "what

we get", "what we want", profit maximizing quantity,

underallocation of resources, overallocation of resources,

consumer surplus, producer surplus, deadweight loss

Market Equilibrium

Changes in Demand and Supply and the Effects

on Equilibrium P and Q

Market Equilibrium is

Efficient

MSB = MSC Model

Maximum Consumer + Producer Surplus

Model

- Shifting

Demand and Supply- Econ 2.3

[4:49 YouTube ACDC Leadership]

- Double

Shifts- Econ 2.5 (Technical Tuesday)

[3:26 YouTube ACDC Leadership]

- Micro

4.13 Dead Weight Loss- Key Graphs of

Microeconomics

[4:45 YouTube ACDC Leadership]

- Micro

2.7 Consumer and Producer Surplus and Dead Weight

Loss

[3:42 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 5a: Government Interference in

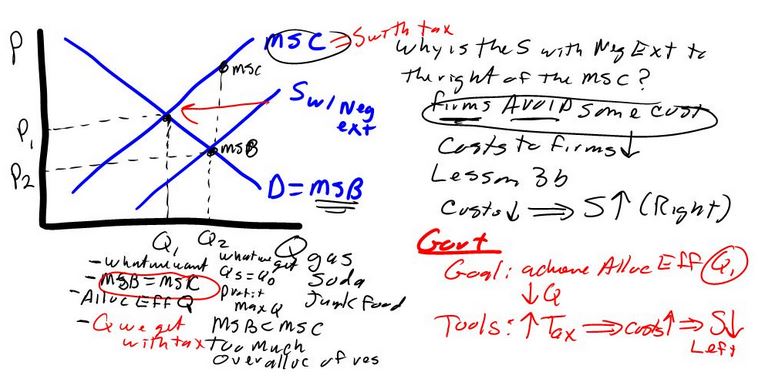

Markets and Market Failures (Negative

Externalities)

In lesson 3c we learned that competitive markets

are efficient and we learned two models to show that markets are

efficient: (1) MSB = MSC, and (2) maximum consumer plus producer

surplus. You must understand these models to understand chapter 5. In

chapter 5 we learn that SOMETIMES markets are NOT

efficient.

When are product markets not

efficient?

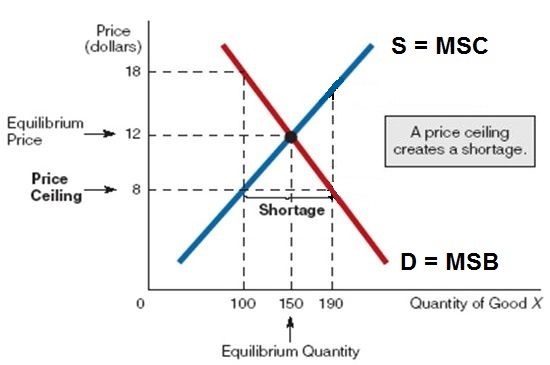

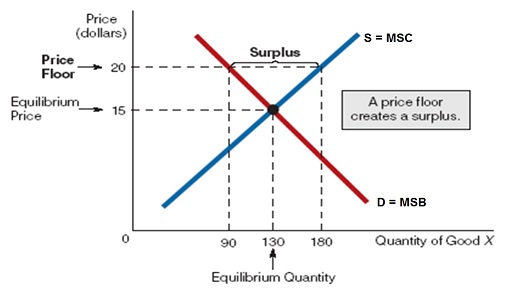

1. when the government sets the price

(price ceilings and price floors - lesson 5a, chapter

3)

2. when the supply curve does not include all

of the costs of producing or consuming the product (negative

externalities - lesson 5a, chapter 5)

3. when the demand curve does not include all of the benefits of

consumption (positive externalities - lesson 5b, chapter 5)

4. when the products are "public goods" (lesson 5b, chapter

5).

5. when there is not competition (monopolies and oligopolies -

chapters 10 and 11)

In this lesson we also will begin our look at

the role of the government in a market economy. This would be a good

time to review chapter 2. In chapter 2 we learned that there is a

limited role for government in market economies. We learned in lesson

3c that markets are efficient, so there is little need for the

government. In this lesson we will see what happens if the government

interferes in markets. We will learn that sometimes governments will

set prices (price ceilings and price floors), rather than letting the

market set the price. In other words: SOMETIMES GOVERNMENTS CAUSE

ALLOCATIVE INEFFICIENCY. (This is the plywood after a hurricane

example discussed in the 5Es reading in lesson 1b.)

Then we will begin to look at examples of when

the markets on their own fail to achieve allocative efficiency and

examine what the government can do to correct these market failures.

SOMETIMES MARKETS BY THEMSELVES ARE INEFFICIENT and the government

may try to modify the market to help it achieve allocative

efficiency. There are three MARKET FAILURES that we will look at in

chapter 5. A "market failure" occurs when the market fails to achieve

allocative efficiency. In lesson 5a we look at the market failure

caused by negative externalities - when the supply curve does not

include all of the costs to society of producing and consuming the

product. Then in lesson 5b we look at the market failures caused by

positive externalities and public goods.

We will assume that businesses will always

produce the profit maximizing quanitity since their goal is to

maximize profits. The profit maximizing quantity is also the

equilibrium quantity that we studied in chapter 3, when the Qs = Qd.

This is WHAT WE GET. We get whatever they produce and they will

produce the quantity that gives them the biggest profits. The goal of

business is not to be efficient. Their goal is to maximize their

profits. If a business can make larger profits by being inefficient

then they will be inefficient. Or if they can make larger profits by

being efficient they they will be efficient. The main point is that

efficiency is not their goal, rather, maximizing profits is their

goal.

The allocatively efficient quantity is what

society wants. We learned at the end of chapter 3 that allocative

efficiency occurs at the quantity where MSB = MSC. This is WHAT WE

WANT. We want to maximize our satisfaction and we learned in chapter

1 that this occurs when we achieve the 5 Es. Allocative efficiency is

one of the 5 Es.

When the profit maximizing quantity equals the

allocatively efficient quantity then markets are efficient . This

means that profit maximizing businesses are producing the quantity

that maximizes society's satisfaction. WHAT WE GET = WHAT WE WANT.

This is the INVISIBLE HAND of capitalism that was discussed in

chapter 2. It's as if there is an invisible hand guiding businesses

to not only make decisions that maximize their profits, but also to

maximize society's satisfaction. As if they don't even know it is

happening.

When markets fail to achieve allocative

efficiency, the profit maximizing quantity (WHAT WE GET or the

equilibrium quantity from chapter 3) is not the same as the

allocatively efficient quantity (WHAT WE WANT or the quantity where

MSB=MSC). Since one of the economic goals of government is to help

the economy achieve efficiency, governments often get involved to

correct for market failures. If the market produces too much

(negative externalities cause allocative inefficiency because of an

overallocation of resources) the government tries to get it to

produce less. If the market produces too little (positive

externalities and public goods causing allocative inefficiency

resulting in an underallocation of resources) the government tries to

get it to produce more.

5a Something Interesting - Why are we

studying this?

|

Cities, states, and countries are debating

whether to add taxes, or raise taxes, on gasoline, soda, and junk

food. Why? Why would it be good for society to raise these taxes?

Below are a small sample of the many news

articles about these taxes

Why gasoline prices might be too

low:

http://www.npr.org/templates/story/story.php?storyId=4858826

Soda Is

About To Get Pricier For Another 5 Million Americans

[Huffington Post, 1/11/2016 03:12 pm ET, Joseph

Erbentraut]

http://www.huffingtonpost.com/entry/cook-county-soda-tax_us_58250427e4b0c4b63b0c0fe4

Why

Mexico taxes junk food and soda:

http://www.politico.com/story/2014/01/mexico-soda-tax-101645

After studying this lesson you should be able

to discuss how negative externalities associated with these

products are the reasons for such taxes and illustrate the effects of

negative externalities on a demand and supply graph.

You should understand why many people support

these taxes.

Chapter 3: pp 61-64, "Application: Government Set

Prices"

Audio:

http://www.marketplace.org/topics/wealth-poverty/fast-food-strike-walk-outs-and-drive-throughs

Chapter 3:

pp 62-63, "Last Word: A Legal Market for Human Organs?"

Chapter 5:

pp 104-110, "Externalities" and "Government's Role in the

Economy

Read:

http://economics.about.com/od/externalities/ss/A-Negative-Externality-on-Production.htm

Read:

https://www.yaleclimateconnections.org/2017/10/mexico-launches-a-carbon-market/

Lecture

Outline

5a Assignments: Video

Lectures

|

GOVERNMENT INTERFERENCE IN MARKETS: Price

Ceilings and Floors

2.5.1 Understanding

How Price Controls Damage Markets

9:38 [MyNotes]

2.5.2 Understanding

the Problem of Minimum Wages in Labor

Markets 14:47 [MyNotes]

Determining

the Effects of Price Ceilings and Price

Floors (econclassroom.com

12:04)

MARKET

FAILURE:NEGATIVE EXTERNALITIES

EconMovies

7: Anchorman (Efficiency and Market Failures)

8.4.1 Defining

Externalities 5:46

[MyNotes]

8.4.2

Explaining

How to Internalize External Costs

(Negative Externalities) 11:58 [MyNotes]

8.5.1

Finding

a Market Solution to External Costs

12:21 [MyNotes]

Negative

Externalities of Production

(econclassroom.com 13:02)

8.5.2

Finding

a Negotiated Settlement to an External Cost -- the Coase

Theorem 12:45 [MyNotes]

8.5.3 Applying

the Coase Theorem 7:02 [

[MyNotes]

5a Outcomes - What you should

learn

|

TOPICS

- Price Ceilings

- Price Floors

- Negative Externalities

OUTCOMES

Price ceilings and floors

- define price ceiling and give

examples

- how do price ceilings affect allocative

efficiency (too little being produced; underallocation of

resources), explain using the MSB=MSC model and the consumer

and producer surplus (dead weight loss) model

- what other effects do price ceilings

have?

- what happens if the government sets a

price ceiling rate that is lower than the

equilibrium?

- define price floor and give examples

- explain the efficiency effects of a

price floor using the MSB=MSC model and show on a graph (too

much being produced; overallocation of resources)

- what happens if the government sets a

price floor that is higher than the equilibrium?

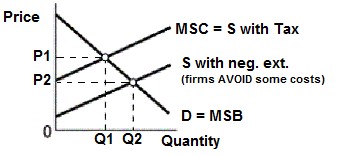

Market Failure: negative externalities (also

called external costs or spillover costs)

- what is a market failure?

- what is an externality?

- define negative externalities (external

costs or spillover costs)

- give examples of negative

externalities

- use the MSB=MSC model to show the effects

(overallocation) on allocative efficiency of negative

externalities

- what can the government do to correct the

market failure caused by negative externalities and show the

effects of these policies on the MSB=MSC model

- Supply is usually equal to MSC, but when

there are negative externalities the supply curve is to the right

of the MSC curve. Why?

- what is an excise tax?

- Why gasoline prices might be too low:

http://www.npr.org/templates/story/story.php?storyId=4858826

- Soda Is About To Get Pricier For Another 5

Million Americans [Huffington Post, 1/11/2016 03:12 pm ET,

Joseph Erbentraut]

http://www.huffingtonpost.com/entry/cook-county-soda-tax_us_58250427e4b0c4b63b0c0fe4

- Why Mexico taxes junk food and soda:

http://www.politico.com/story/2014/01/mexico-soda-tax-101645

- what is the Coase theorem?

- explain how according to the Coase Theorem

that under certain circumstances bargaining can solve the problems

created by negative externalities without the government using an

example

- what are the necessary condition needed for

the Coase Theorem to work?

- what is the tragedy of the

commons?

- how does the tragedy of the commons affect

allocative efficiency?

- what can be done to better achieve

allocative efficiency when there is a tragedy of the

commons?

Key Terms

Flash Cards - Click Here

Key Terms:

price ceiling, rent controls, price

floor, market failure, externality, negative externality (external

cost, spillover cost), internalizing the externality, excise tax,

incidence of a tax, cap and trade, Coase Theorem

Negative

Externalities

Click on the link above to learn how to use a

supply and demand graph to show the economic effect of negative

externalities.

Price Ceiling (causes a shortage)

Price Floor (causes a surplus)

Negative Externality

Negative Externality and Taxes

- Price

Ceilings and Floors- Economics 2.6

[4:34 YouTube ACDC

Leadership]

- Pollution,

the Government, and MSB=MSC- Microeconomics

6.2

[3:25 YouTube ACDC Leadership]

- Micro

6.3 Negative Externalities: Econ Concepts in 60

Seconds-Externality

[2:31 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 1: Markets are Efficient, Except

. . . Intro to Microeconomics

Lesson 5b: Market Failures Continued

(Positive Externalities and Public Goods)

We have learned that competitive markets are

usually efficient. This is one of the benefits of a market economy or

capitalism (chapter 2) . But sometimes even markets can be

allocatively inefficient. In lesson 5a we learned that when negative

externalities exist, a market will produce too much of a good or

service (an overallocation of resources) and therefore the government

should tax the product (like gasoline taxes) to get consumers to buy

less, i.e. without the tax the price of gasoline is too

low.

In this lesson we will look at two other market

failures, but this time the market produces too little (an

underallocation of resources) because the demand curve for the

product does not include all of the benefits. This occurs when there

are positive externalities and when there are "public goods". Be

careful - remember - economists often change the definitions of

words. Public schools and a public parks are not public goods

according to our definition. Since markets produce too little when

there are negative externalities or public goods, the goal of

government is to increase production.

In later chapters (10 and 11) we will discuss

another market failure: the lack of competition. If a market is not

competitive, like when it is a monopoly or an oligopoly, then profit

maximizing businesses will produce less than the allocatively

efficient amount. The invisible hand of capitalism does not work well

if the market is not competitive.

5b Something Interesting - Why are we

studying this?

|

Why does the government do what it does?

Governments in the United States, build and run schools, libraries,

and parks, but not gas stations, clothing stores, or grocery stores?

Why some things and not other things? Does it make sense or is it

just random?

We have learned that competitve markets achieve

efficiency, both allocative and productive. And we learned that

competitive markets have a limited role for government. So why does

the government do schools, libraries, and parks, and we could add

roads, bridges, airports, football stadiums, and vaccinations. Why

these things and not other things? Why not let private businesses do

these things like they do gas stations, clothing stores, and grocery

stores?

If markets are efficient, then, if the

government is doing something rather than the market, WE SHOULD ASK,

WHY?

In this lesson you will learn two reasons that

explain much of why the government does what it does: POSITIVE

EXTERNALITIES and PUBLIC GOODS.

One other interesting question: public schools,

public libraries, and public parks ARE NOT PUBLIC GOODS. Why

not?

Chapter 5: pp 99-110, "Public Goods",

"Externalities" and "Government's Role in the Economy"

Lecture

Outline

5b Assignments: Video

Lectures

|

MARKET FAILURE: POSITIVE EXTERNALITIES

8.4.3 Explaining

How to Internalize External Benefits (Positive

Externalities (5:34)

[MyNotes]

Market

Failure - Positive Externalities of

Consumption (econclassroom.com

10:51)

MARKET FAILURE: PUBLIC GOODS

8.2.1 Defining

Public Goods 13:32

[MyNotes]

The

Tragedy of the Commons as a Market Failure

(econoclassroom.com 14:29) [MyNotes]

Tragedy

of the Commons (YouTube -

LearnLiberty - 3:19)

5b Outcomes - What you should

learn

|

TOPICS

- positive externalities

- public goods

- tragedy of the commons

OUTCOMES

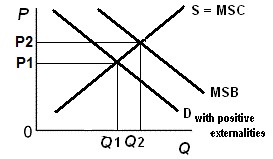

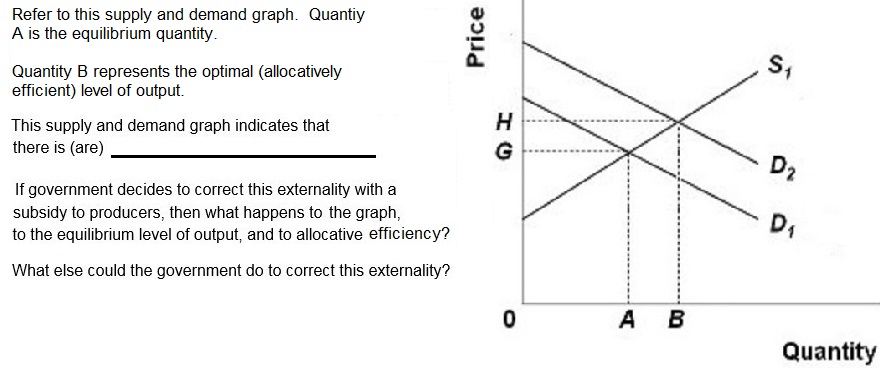

Market Failure: positive externalities (also

called external benefits or spillover benefits)

- define positive externalities (external

benefits or spillover benefits)

- give examples of positive

externalities

- use the MSB=MSC model to show the effects

on allocative efficiency of positive externalities

- what can the government do to correct the

market failure caused by positive externalities and show the

effects of these policies on the MSB=MSC model

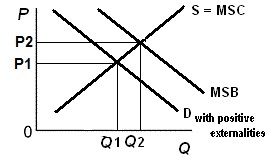

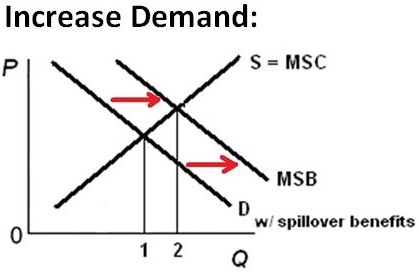

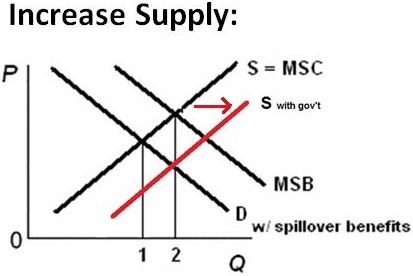

- Demand is usually equal to MSB, but when

there are positive externalities the demand curve is to the left

of the MSB curve. Why?

- Are positive externalities (spillover

benefits) good or bad for society? Why or why not?

- Comment on: EconMovies

7: Anchorman (Efficiency and Market Failures)

http://www.youtube.com/watch?v=FBjFDtH-iZM

Market Failure: Public Goods

- define "public goods (public goods are

non-exclusive and non-rival)"

- give examples of public goods and explain

why they are public goods

- define private (exclusive) goods" and give

examples

- define "rival goods" and give

examples

- what is the "free rider

problem"?

- explain how to derive the demand curve for

public goods

- what effect do public goods have on

allocative efficiency?

- what can the government do to correct for

the market failure of public goods?

- Why are public schools, public parks, and

public libraries NOT "public goods"? If they are not public goods

then why does the government produce them?

Market Failure: Tragedy of the

Commons

- what is the Tragedy of the Commons (common

access resources are non-exclusive but rival)

- how does the tragedy of the commons affect

allocative efficiency?

- what can be done to better achieve

allocative efficiency when there is a tragedy of the

commons?

Key Terms

Flash Cards - Click Here

Key Terms:

positive externalities (external

benefits or spillover benefits), private goods, public goods,

rivalry (rival goods), nonrival goods, excludability (exclusion

principle, exclusive goods), nonexcludability, (nonexclusive

goods), free-rider problem, benefit-cost analysis

(marginal-cost-marginal-benefit rule), tragedy of the commons,

common access resources

The

Economic Effects of Positive Externalities

Click on the link above to learn how to do this

problem.

Positive Externalities

Positive Externalities and the Role of

Government: Increase Demand

Positive Externalities and the Role of

Government: Increase Supply

- Micro

6.4 Positive Externalities- ACDC Econ

[2:42 YouTube ACDC Leadership]

NOTE: These are REVIEW videos only. In order to

learn the material you must read the assigned textbook readings,

watch the assigned lecture videos, and do problems. See the LESSONS

link on Blackboard for these assignments.

Unit 2: Elasticity, Consumer Choice,

Costs

Lesson 4a: Price Elasticity of Demand

and Tax Incidence

We learned in chapter 3 that when the price of

pizza goes up the quantity demanded goes down. (What happens to

demand? . . . . NOTHING.) So we know when the price of a product goes

up then the quantity demanded goes down and when the price goes down

the quantity demanded goes up. We called this the "law of demand" in

chapter 3. What we are going to learn in chapter 4 is HOW MUCH?

If the price of pizza goes up, HOW MUCH

less will we buy? A LITTLE less or A LOT less? The price

elasticity of demand will answer this question and it will also

explain why farm incomes were high during a year of a record drought

and were low during a year of a record harvest.

You already understand elasticity. Think about

this:

if the price of gasoline goes up HOW MUCH less

will consumers buy? A little less or a lot less?

I believe most students will say A LITTLE less.

If the price of a Big Mac goes up, HOW MUCH

less will consumers buy? A little less or a lot less?

I bet most of you answered A LOT less.

If the price of salt goes up, how much less

will consumers buy? A little less or a lot less?

Correct. Only A LITTLE less.

If the price of a new car goes up, how much

less will consumers buy? A little less or a lot less?

A LOT less.

The price elasticity of demand measures

how responsive consumers are to changes in prices. Don't confuse

elasticity with the law of demand. The law of demand tells us that

when prices go up, the quantity demanded will go

down. Elasticity tells us HOW MUCH it will go down.

Chapter 3 - law of demand:

if the P

Qd

Chapter 4 - price elasticity of

demand:

if the P

does Qd or Qd

or Qd  ?

?

if price changes, HOW MUCH will the Qd change? A little or a

lot?

In chapter 3 we learned the direction of the

arrows (up or down). In chapter 4 we learn the size of the arrows

(big or small).

4a Something Interesting - Why are we

studying this?

|

In 2012 there was a severe drought in the US corn

growing region. In 2014 the weather was great and the corn crop was

at a record high. In which year did farmers make the most

money?

They made more in 2012 when the weather was bad

!!!

After studying this lesson you should

understand why good farming weather results in low farm incomes and

bad farming weather results in high farm incomes. Really!

See:

Sept. 2012: Despite

Record Drought, Farmers Expect Banner Year

Sept. 2014: Corn,

soybean crop expected to hit record high -- Great season could

mean bad prices for farmers ("This

year, farming income is expected to drop by 14

percent.")

ANSWER: The answer to this paradox is that the

demand for corn and soybeans is price INELASTIC. You will learn that

bad weather causes the price of crops to increase whch causes farm

incomes to increase and good weather causes the price of farm corps

to decrease causing incomes to decrease BECAUSE THE DEMAND FOR CORN

AND SOYBEANS IS PRICE INELASTIC.

Chapter 4: pp. 75-84,

Chapter 4:

pp 86-87, Last Word

Chapter

16: pp 347-354, "Tax Incidence and Efficiency Loss

Lecture

Outline

4a Assignments: Video

Lectures

|

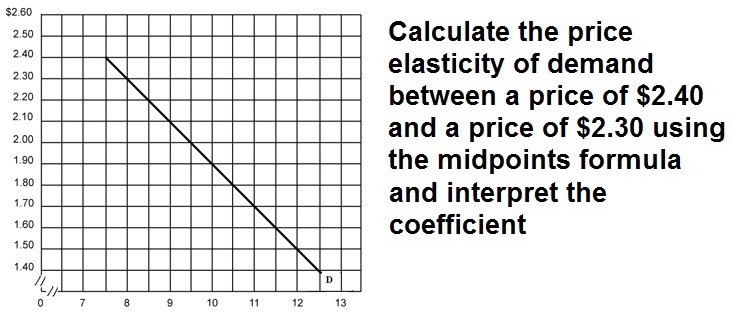

2.4.1 Defining

Elasticity 4:47 [MyNotes]

2.4.2

Calculating

Elasticity 11:43 [MyNotes]

2.4.3

Applying

the Concept of Elasticity 8:42

[MyNotes]

2.4.4

Identifying

the Determinants of Elasticity 6:50

[MyNotes]

2.4.5

Understanding

the Relationship between Total Revenue and

Elasticity 8:09 [MyNotes]

Examining

the Effect of an Excise Tax on an Inelastic Good --