OUTLINE -- CHAPTER 9

Producer Decisions: Benefits (Pure Competition)

[Class Handout: Three Rules and Four Models (.doc)

(.htm)]

I. Benefit-Cost Analysis and Producer Decisions

A. Decision: How Many to Produce:

B. Goal: Maximize Profits

C. Benefit Cost Analysis:

all where: MB > MC

up to where: MB=MC

but never where: MB<MC

II. The Product Market

A. Circular

Flow Model

B. Four Product Market Models

1. Competitive

Market (Ch. 9)

2. Monopoly

(Ch. 10)

3. Monopolistic

Competition (Ch. 11)

4. Oligopoly

(Ch. 11)

C. General Outline for Each Model

1. Characteristics and Examples

2. Nature of the Demand Curve

3. Short Run Equilibrium (Profit Max.)

4. Long Run Equilibrium and Efficiency

5. Other Issues

III. Pure Competition.

A. Definition

A market structure in

which a very large number of firms sell a standardized product

into which entry is very easy in which the individual seller

has no control over the product price and in which there is no

nonprice competition; a market characterized by a very large

number of buyers and sellers.

B. Characteristics of Competitive Markets

1. NUMBER OF FIRMS: very large numbers

2. TYPE OF PRODUCT: standardized product

3. CONTROL OVER PRICE: "price takers"

A seller (or buyer) of

a product or resource who is unable to affect the price at

which a product or resource sells by changing the amount it

sells (or buys).

4. EASE OF ENTRY: free entry

5. NONPRICE COMPETITION: none

C. Examples / Relevance

1. applying benefit cost analysis

2. competitive markets used as the "standard" of efficiency

3. agriculture

D. Demand and Competitive Markets

1. demand faced by the firm is

perfectly elastic

2. market demand is downsloping

IV. Short Run Profit Maximization: Benefit-Cost Analysis

Approach

A. Benefit-Cost Analysis

1. definition

the selection of ALL possible alternatives where

the marginal benefits are greater than the marginal cost

select all where: MB

> MC

up to where: MB = MC

but never where: MB < MC

2. marginal costs = MC (ch. 8)

3. What are the MBs of selling one more unit of output?

marginal benefits =marginal revenue (MR)

a) total revenue (TR = P x Q)

b) MR =  TR /

Q

TR /

Q

B. Profit Maximization -- Applying Benefit-Cost

Analysis

1. step 1: find best quantity (where MR = MC)

2. step 2: are AR > AVC? If yes, then produce this

quantity

3. calculate profits

a) profits = TR - TC

b) check to see if profits are maximized

How

to find the profit maximizing quantity:

A

firm will maximize its profit (or minimize its losses) by

producing that output at which marginal revenue and

marginal cost are equal provided product price is equal

to or greater than average variable cost

(1)

Find the quantity where: MR=MC

(2)

produce this quantity if: AR > AVC

|

C. Three Cases -- using BOTH cost schedules and

graphs

1. profit maximizing case

a) step 1: find quantity where MR = MC

b) step 2: are AR > AVC? If yes, then produce this

quantity

c) calculate profits

d) textbook

graph, graph

2. loss minimizing case

a) step : find quantity where MR = MC

b) step 2: are AR > AVC? If yes, then produce this

quantity

c) calculate profits

d) check to see if losses are minimized

e) why not close down?

f) graph

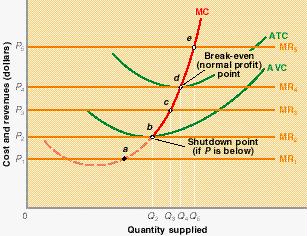

3. shutdown case

a) step 1: find quantity where MR = MC

b) step 2: are AR > AVC? If yes, then produce this

quantity

c) calculate profits/check

d) graph

4. Quick

Review Quiz / Quick

Review Quiz

D. Marginal Cost and the Short Run Supply Curve

- A supply curve

which shows the quantity of a product a firm in a purely

competitive industry will offer to sell at various prices in

the short run;

- the portion of

the firm’s short-run marginal cost curve which lies above

its average variable cost curve.

graph

V. Profit Maximization: total cost minus total revenue

approach

A. Short Run

B. Graphs

VI. Profit Maximization in the Long Run

A. Assumptions

B. LR Equilibrium: competitive markets

1. "After all long-run adjustments are

completed, product price will be exactly equal to, and

production will occur at, each firm's point of minimum average

total cost"

2. zero profit (normal profit) model

C. Why?

1. entry of firms eliminates profits (graph)

From the Textbook:

|

IF DEMAND INCREASES,

PRICE WILL INCREASE

NEW FIRMS WILL ENTER

AND PRICE WILL FALL BACK TO WHERE IT WAS

|

PROFITS WILL RETURN TO NORMAL (ZERO)

|

|

|

|

2. exodus of firms eliminates losses

(graph)

From the Textbook:

|

IF DEMAND DECREASES,

PRICE WILL DECREASE

FIRMS WILL GO OUT OF BUSINESS

AND PRICE WILL RISE BACK TO WHERE IT WAS

|

PROFITS WILL RETURN TO NORMAL (ZERO)

|

|

|

|

D. Pure

competition: Long-run equilibrium graph

F. Long Run Supply Curve

A

schedule or curve showing the prices at which a purely

competitive industry will make various quantities of the

product available in the long run.

1. constant cost industry

An

industry in which expansion or contraction will not affect

resource prices and therefore production costs

Graphically,

it means the entry or exit of firms does not shift the

long-run ATC curves of individual firms

Occurs when

the industry's demand for resources is small in relation to

the total demand for those resources

2. increasing cost industry

An

industry in which expansion through the entry of new firms

increases the prices firms in the industry must pay for

resources and therefore increases their production

costs.

3.

decreasing cost industry

An

industry in which expansion through the entry of firms

decreases the prices firms in the industry must pay for

resources and therefore decreases their production

costs.

VII. Pure Competition and Efficiency !!!!!!!!!!!!!!!!

A. Competitive Markets Used as Standard of

Efficiency

B. Productive Efficiency

1. definition

The

production of a good in the least costly way or

producing at a minimum cost

2. P = minimum ATC (MC=ATC)

productive

efficiency occurs when production takes place at the output at

which average total cost is a minimum

3. Pure

competition: Long-run equilibrium graph

How

to find the productively efficient quantity:

Society

will achieve productive efficiency by producing that

output at which the average total cost (ATC) is at a

minimum

MC

= ATC

|

C. Allocative Efficiency

1. definition

The

apportionment of resources among firms and industries to

obtain the production of the products most wanted by society

(consumers);

2. MSB = MSC

( To review MSB, MSC and Efficiency see

supply, demand, and

economic efficiency from chapter

3 )

3. The allocatively efficient quantity: P = MC

Allocative

efficiency is achieved at the output of each product at

which its marginal cost and price or marginal benefit are

equal (P = MC).

a. MSB =

P

b. MSC = MC

c. Therefore: MSB = MSC where P = MC

4.

Pure

competition: Long-run equilibrium graph

5. allocative inefficiency

a. underallocation of resources: P > MC

b. overallocation of resources: P < MC

How

to find the allocately efficient quantity:

Society

will achieve allocative efficiency by producing that

output at which price and marginal cost are equal

P=MC

|

5. marginal cost pricing

To achieve allocative efficiency: MSB should

equal MSC

If P measures MSB and MC measure MSC then to achieve

allocative efficiency:

P should equal MC

EXAMPLES:

a. all you can eat / free refills

- what are the MSC to society (MC to the firm) of

having one more?

- what is the price (P) to the consumer of having

one more?

- does P=MC (or MSB=MSC) ?

- if not, is P>MC or is P< MC ?

- is allocative efficiency achieved? - or is there

an OVER- or UNDER-allocation of resources?

b. electricity rates

- summer vs. winter

- when is the MC higher?

- therefore, to achieve allocative efficiency,

when should the price be higher?

- if the price is not higher what might

happen?

- days vs. evening (making snow only at night -

why?)

- Why do they only make snow at night?

- when is the MC lower?

- therefore, to achieve allocative efficiency,

when should the price be lower?

c. plane fares

- what is the MC of adding one more traveler to a

plane that is half full?

- what is the MC of adding one more traveler to a

plane is is full?

- Why do they charge less for "standby"?

- Is this efficient?

d. rent with utilities included

- what are the MSC to society (MC to the firm) of

turning the heat up in the winter?

- what is the price (P) to the consumer of turning

the heat up in the winter?

- does P=MC (or MSB=MSC) ?

- if not, is P>MC or is P< MC ?

- is allocative efficiency achieved or is there an

OVER- or UNDER-allocation of resources?

e. bus fares

- when is the cost (MC) to the bus company, or the

cost to society (MSC), greater?

- at rush hour ?

- or at noon hour ?

- when should the price be higher to achieve

allocative efficiency?

f. parking meters

- when is the cost to society (MSC) of allowing one

more person to park greater?

- week days when there are few or no available

parking spaces?

- weekends when there are many available parking

spaces?

- when should the price be higher to achieve

allocative efficiency?

- what should the price be on weekends to be

allocatively efficient assuming that there are very many

empty parking spaces available?

g. garbage collection and recycling

h. tollway fares

- when is the cost to society (MSC) of allowing one

more car on the tollway greater?

- rush hour when there is a lot of

traffic?

- noon hour when there is very little

traffic?

- when should the price be higher to achieve

allocative efficiency?

- how does this save resources?

i. external costs anad external benefits (spillover

costs and benefits) (see chapters 4 and 16)

j. other

D. Dynamic Adjustments / dynamic efficiency

VIII. Qualifications (Shortcomings) of the Competitive

Price System

A. Income Distribution Problems (Equity)

B. Market Failures: Spillovers and Public Goods

C. Productive Techniques

1. natural monopolies

2. technological progress (Dynamic Efficiency)

a. incentive

b. means

D. Range of Consumer Choice

{kind=link}

{kind=link}

{kind=link}