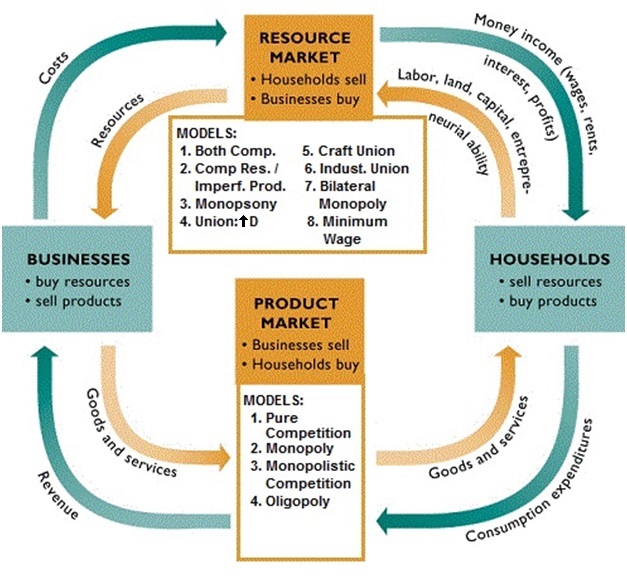

OUTLINE - Chapter 12

– The Demand for Resources

12a

Brief Outline:

<![if !supportLists]>·

<![endif]>4 reasons to study the

resource markets

<![if !supportLists]>·

<![endif]>The strength of resource

demand depends on two things

<![if !supportLists]>·

<![endif]>Find the profit

maximizing quantity of resources to employ: MRP = MRC

<![if !supportLists]>·

<![endif]>Find the resource demand

curve: MRP

<![if !supportLists]>·

<![endif]>The first two (of eight)

resource market models

<![if !supportLists]>o

<![endif]>Pure competition in both

the resource and product markets

<![if !supportLists]>o

<![endif]>Pure competition in the

resource market and imperfect competition in the product market

<![if !supportLists]>o

<![endif]>Compare the profit

maximizing quantity (where MRP=MRC) with the allocatively

efficient quantity: (VMP = W or P x MP = W)

<![if !supportLists]>·

<![endif]>Determinants

of Resource Demand

<![if !supportLists]>o <![endif]>Changes in Demand for the Product (Pe, Pog, I, Npot,

Tastes)

<![if !supportLists]>o <![endif]>Changes in the Productivity of the

Resource

<![if !supportLists]>o <![endif]>Changes

in the Prices of Other Resources

<![if !supportLists]>§ <![endif]>Substitutes

<![if !supportLists]>§ <![endif]>Complements

<![if !supportLists]>·

<![endif]>Price

Elasticity of Resource Demand - Determinants

<![if !supportLists]>o <![endif]>Ease of resource substitutability

<![if !supportLists]>o <![endif]>Elasticity of product demand

<![if !supportLists]>o <![endif]>Ratio of resource cost to total cost

Long Outline:

Significance of Resource Demand

- Income determination

- Cost minimization

- Resource allocation

- Policy Issues

Marginal Productivity Theory of Resource Demand

Define: Resource

Demand

Define: Derived Demand

The

strength of the resource demand for resources depends on two factors:

1. The productivity of the resource in

helping to create a good or service.

<![if

!supportLists]>·

<![endif]>a resource that is

highly productive in turning out a highly valued commodity will be in

great demand

<![if !supportLineBreakNewLine]>

<![endif]>

2. The market value or price of the good or

service it helps produce.

<![if

!supportLists]>·

<![endif]>a resource that is used

to produce highly valued product will be

in great demand

Review:

Total Product (TP)

Marginal Product (MP)

Define

MRP

Rule

for Employing Resources: MRP =MRC

12a

<![if

!supportLists]>·

<![endif]>to

maximize profits employ all where the MRP>MRC, up to where MRP=MRC

<![if

!supportLists]>·

<![endif]>this

is just benefit cost analysis: MB = MC

<![if

!supportLists]>o

<![endif]>what is the

marginal benefit to the firm of hiring one more worker? = MRP

<![if

!supportLists]>o

<![endif]>what is the

marginal cost of hiring one more worker? = MRC

How to find the resource demand curve:

<![if

!supportLists]>·

<![endif]>Review:

Demand is a schedule that shows the various quantities that will be

hired at various wage rates

<![if

!supportLists]>·

<![endif]>Firms

will hire the profit maximizing quantity

<![if

!supportLists]>·

<![endif]>So,

all we have to do is find the profit maximizing quantities of labor

at different wage rates

Value

of the Marginal Product (VMP = Product Price x MP)

<![if

!supportLists]>·

<![endif]>The value of marginal

product is the value to society of a firm hiring one more unit of a

factor of production.

<![if

!supportLists]>·

<![endif]>This is the MSB of

hiring another workeer

<![if

!supportLists]>·

<![endif]> The

value of marginal product equals the price of a unit of output

multiplied by the marginal product of the factor of production. P x

MP = VMP

_______________________________________________________________________________

NOT IN THE TEXTBOOK:

Rule for finding the allocatively efficient

quantity to hire: VMP = W

or PxMP=W

<![if

!supportLists]>·

<![endif]>So, what quantity of

a resource should be hired to maximize society’s satisfaction? (allocative efficiency)

<![if

!supportLists]>o

<![endif]>The

quantity where MSB = MSC

<![if

!supportLists]>o

<![endif]>VMP

= MSB

<![if

!supportLists]>o

<![endif]>W

= MSC

<![if

!supportLists]>o

<![endif]>So

the best quantity of a resource to hire for society is where:

VMP = W or PxMP = W

<![if

!supportLists]>§ <![endif]>This is similar to the product market

where P=MSB and MC=MSC, so the best quantity of a product to

produce for society was where: P=MC

_______________________________________________________________________________

Competitive

Model:

12a

Assume perfect competition in the product market

<![if

!supportLists]>·

<![endif]>product

price is constant because each firm produces such a small fraction of

the total market supply of the product (chapter 8)

<![if

!supportLists]>·

<![endif]>means

they can sell all they want without having to lower the price

<![if

!supportLists]>·

<![endif]>therefore

in the product market: P=MR

Assume: perfect competition in the labor market

<![if

!supportLists]>·

<![endif]>wage

(resource price) is constant because each firm hires such a small

fraction of the total market supply of workers

<![if

!supportLists]>·

<![endif]>means

they can hire all they want without having to offer higher wages

<![if

!supportLists]>·

<![endif]>therefore

in the competitive labor market: W=MRC

<![if !vml]> <![endif]><![if !vml]>

<![endif]><![if !vml]> <![endif]>

<![endif]>

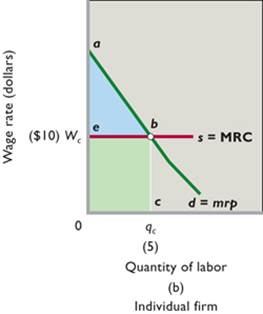

MRP is the Resource Demand Curve

MRP also equals VMP if the product market is competitive

So qc is the profit

maximizing quantity to hire AND the allocatively

efficient quantity to hire.

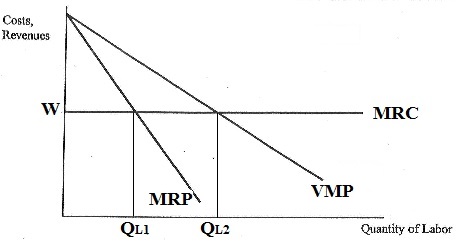

Imperfect

Product Market and Resource Demand:

12a

Assume imperfect competition in the product market (monopoly,

oligopoly, monopolistic competition)

<![if

!supportLists]>·

<![endif]>downward

sloping product demand curve

<![if

!supportLists]>·

<![endif]>means

they must lower their price to sell more

<![if

!supportLists]>·

<![endif]>therefore

in the product market P > MR

Assume: perfect competition in the labor market

<![if

!supportLists]>·

<![endif]>wage

(resource price) is constant because each firm hires such a small

fraction of the total market supply of workers

<![if

!supportLists]>·

<![endif]>means

they can hire all they want without having to offer higher wages

<![if

!supportLists]>·

<![endif]>therefore

in the competitive labor market: W=MRC

<![if !vml]> <![endif]>

<![endif]>

<![if

!supportLists]>o

<![endif]>QL1 is the quantity hired if the product market is imperfect

<![if

!supportLists]>o

<![endif]>QL2 is the quantity hired by a perfectly competitive producer

<![if

!supportLists]>o

<![endif]>We know a monopoly will maximize

profits by producing less output than a competitive producer, here we

see that they will also hire fewer workers

Market

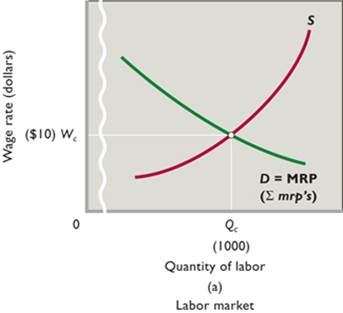

Demand for a Resource: horizontal summation

Determinants of Resource Demand

<![if !supportLists]>·

<![endif]>Changes

in Demand for the Product (determinants: Pe,

Pog, I, Npot, Tastes)

<![if !supportLists]>·

<![endif]>Changes

in the Productivity of the Resource

<![if !supportLists]>·

<![endif]>Changes in the Prices of

Other Resources

<![if !supportLists]>o <![endif]>Substitutes

<![if !supportLists]>o <![endif]>Complements

<![if !supportLists]>·

<![endif]>Changes

in Demand for the Product

<![if !supportLists]>o <![endif]>Other

things equal, an increase in the demand for a product will increase

the demand for a resource used in its production, whereas a decrease

in product demand will decrease the demand for that resource.

<![if !supportLists]>o <![endif]>Pe, Pog, I, Npot,

T

12a

<![if !supportLists]>·

<![endif]>Changes in the

Productivity of the Resource

<![if !supportLists]>o <![endif]>Other

things equal, an increase in the productivity of a resource will

increase the demand for the resource and a decrease in productivity

will reduce the demand for the resource.

<![if !supportLists]>o <![endif]>Productivity

depends on:

<![if !supportLists]>§ <![endif]>Quantity of other resources used by

the labor

<![if !supportLists]>§ <![endif]>The

greater the amount of capital and land resources used with, say,

labor, the greater will be labor's marginal productivity

and, thus, labor demand.

<![if !supportLists]>§ <![endif]>Quality of the Labor

<![if !supportLists]>§ <![endif]>Improvements

in the quality of the variable resource, such as labor, will increase

its marginal productivity and therefore its demand.

<![if !supportLists]>§ <![endif]>Technological Advance (Quality of

Capital used by labor)

<![if !supportLists]>§ <![endif]>The

better the quality of capital, the greater the productivity of

labor used with it and therefore its demand.

<![if !supportLists]>·

<![endif]>Changes in the Prices of

Other Resources

<![if !supportLists]>o <![endif]>Substitutes

(Warning: this can be confusing.)

<![if !supportLists]>§ <![endif]>A

decrease in the price of one resources may INCREASE (output

effect) or

DECREASE (substitution effect) demand

for its substitute

<![if !supportLists]>§ <![endif]>Substitution

Effect (a decrease in the price of one resource will decrease the

demand for its substitute)

<![if !supportLists]>§ <![endif]>The

decline in the price of machinery prompts the firm to substitute

machinery for labor. This allows the firm to produce its output at

lower cost. So at the fixed wage rate, smaller quantities of labor

are now employed. This substitution effect decreases

the demand for labor.

<![if !supportLists]>§ <![endif]>Output

Effect (decrease price of one resource increases the demand for

its substitute)

<![if !supportLists]>§ <![endif]>Because

the price of machinery has fallen, the costs of producing various

outputs must also decline. With lower costs, the firm finds it

profitable to produce and sell a greater output. The greater output

increases the demand for all resources, including labor. So this

output effect. increases the demand for labor.

<![if !supportLists]>o <![endif]>Complements

<![if !supportLists]>§ <![endif]>If

resources are complements, then they must be used together (like one

worker per machine)

<![if !supportLists]>§ <![endif]>an increase in the quantity of one of them used

in the production process requires an increase in the amount used of

the other as well, and vice versa.

<![if !supportLists]>§ <![endif]>So

if the price of a machine goes down the firm will buy more machines

and this will increase the demand for labor needed to run the

machines

<![if !supportLists]>·

<![endif]>Summary

of Changes in Resource Demand: the demand for labor

will increase (the labor demand curve will shift rightward)

when:

<![if !supportLists]>o

<![endif]>The demand for (and

therefore the price of) the product produced by that labor

increases.

<![if !supportLists]>o

<![endif]>The productivity (MP) of

labor increases.

<![if !supportLists]>o

<![endif]>The price of a

substitute input decreases, provided the output effect exceeds

the substitution effect.

<![if !supportLists]>o

<![endif]>The price of a

substitute input increases, provided the substitution effect

exceeds the output effect.

<![if !supportLists]>o

<![endif]>The price of a

complementary input decreases.

Price Elasticity of Resource Demand

12a

<![if !supportLists]>·

<![endif]>Review

Elasticity

<![if !supportLists]>·

<![endif]>Define

<![if !vml]> <![endif]>

<![endif]>

<![if !supportLists]>·

<![endif]>Determinants

<![if !supportLists]>o <![endif]>Ease of resource substitutability

<![if !supportLists]>§ <![endif]>If there are many substitute

resources, demand for the resource is MORE ELASTIC

<![if !supportLists]>o <![endif]>Elasticity of product demand

<![if !supportLists]>§ <![endif]>If demand for the product is more

elastic, then demand for the resource is MORE ELASTIC

<![if !supportLists]>o <![endif]>Ratio of resource cost to total cost

<![if !supportLists]>§ <![endif]>If the resource cost is a large

fraction of the total costs then demand for the resource is MORE

ELASTIC

Marginal

Productivity Theory of Income Distribution

<![if !supportLists]>9. <![endif]>Minimum

Wage

<![endif]>

<![endif]>